Livin' La Vida Luna

Jean Jacket ✔️

Rainbow Capris ✔️

Slay Everyday ✔️

Property 4: We Bought a Duplex

We closed on a duplex in Madison, NJ. There were many bumps along the way, but it should all be worth it.

We have three exit strategies for this acquisition and I can’t wait to see how this all pans out.

📖 Quick Background

A few months ago, I cold-called the listing agent for this property.

However, the listing I called wasn’t a property for sale on Zillow or the MLS. It was a Craigslist rental listing for a 3 bed 2 bath apartment in a side by side duplex.

My intention behind calling rental listings is to find a tired landlord sitting on a vacant unit. In my head, that makes for a highly motivated seller.

My logic panned out.

🏡 The Property

Features:

- 2,200 Square Feet

- Unit 1: 3 beds, 2 baths

- Unit 2: Studio, 1 bath

- Separate utilities

- Separate basements

- Roof and Mechanicals in Healthy Condition

- No Oil Tank

Benefits:

- Decent Condition - No immediate work required

- 10-minute walk to a train station that goes to NY Penn

- Quiet street on the edge of downtown

- Off-Street Parking for ~4 cars

🔢 The Numbers

- Purchase Price: $485,000

- Property Taxes: $8,300 / year

- Insurance: $1,700 / year

- Unit 1 Rent: Currently Vacant

- Unit 2 Rent: $1,000 / month with lease expiring on 8/31/2021

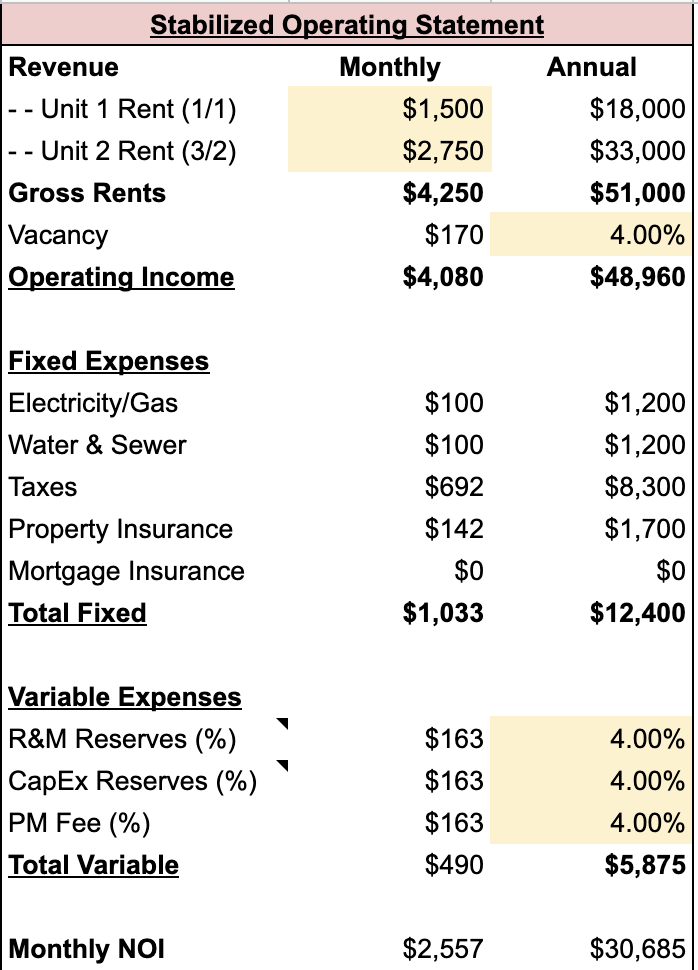

🧮 The Pro-Forma:

According to the Small Area Fair Market Rent Tool, stabilized rents are:

- Unit 1: $2,790 - We’re using $2,750

- Unit 2: $1,510 - We’re using $1,500

The tenants are separately metered and pay their own utilities. The common area utility expenses will be minimal. We factored in $50 per month for each utility.

Once the rental income is stabilized, this property should generate $2,500 per month in Net Operating Income.

🥇 Exit Strategy 1

This is less of an exit strategy and more of a monetization strategy.

We improve the vacant unit with a new kitchen and new baths and rent it out at $2,750 per month.

Once the studio lease is up at the end of August, we can improve that unit as well with a new kitchen and bath and rent it out at $1,500 per month.

These improvements will cost ~$30,000:

- $15,000 for both kitchens

- $15,000 for three bathrooms.

We would then refinance the property and put a new loan of $420,000, which leaves ~$95,000 of cash in the deal.

Although we’d cashflow $500/mo, I don’t love leaving money in deals, so let’s move on to option number 2.

🥈 Exit Strategy 2

We exit the property in its as-is condition.

We immediately turn around and list this property for sale. This was an “off-market” acquisition and we believe we got a healthy discount.

If we list it as is, we believe it can sell for a minimum of $550K. We are testing the market with this approach right now.

$550K - $485K = $65K in gross profit. That will probably dwindle to $50K after all fees associated with the sale.

At this price, the right buyer stands to make a killing. Allow me to paint a picture.

Let’s say a young couple with or without one child decides to buy this duplex to live on one side and rent out the other.

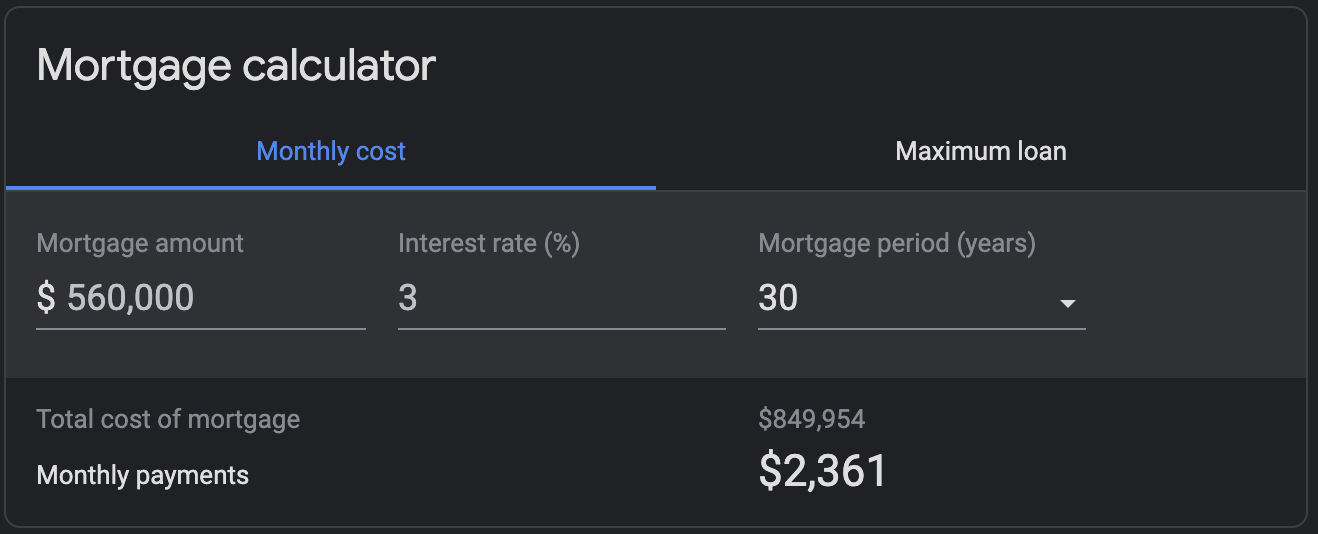

They buy this property using a 203K Loan. They put 3.5% down on $550,000 and add on a $30,000 loan for repairs. Their total cost-basis would be $580,000.

So that’s $20,000 down and a loan amount of $560,000 at 3% fixed over 30 years.

Their mortgage payment would be $2,361 per month for principal and interest only. If you add in property taxes and insurance, their monthly payment would be closer to $3,200.

As they live there, the studio tenant would reduce their cost of living by $1,500 per month. So they’d be living in a 3 bed 2 bath unit in Madison, NJ for $1,700 per month. So far so good, but it gets better.

Once they move on to bigger and better things, they’ll have a cash-flowing asset because the unit they’re living in will rent out for $2,750 per month. So they’ll go from paying $1,700 to live there to getting paid $1,050 per month to not live there.

The best part is there’s no need to worry about PMI. Once the $30,000 of improvements are made to this property, it could be worth up to $700,000, but let’s say $650,000 to be conservative.

A $650,000 value means they’ll have the 20% equity required to do a Streamline refinance out of their PMI loan into a loan without PMI.

Solid deal, right? If you know someone who wants to bring my painting to life, please let me know!

🥉 Exit Strategy 3

We improve the property ourselves and then exit. If we can’t sell for $550K before 8/31/2021, we’ll likely go down this third and final route.

We’ll go ahead and make the $30K of improvements to the kitchens and baths ourselves. Then market the property for $650K.

I’d rather not go down this route because our carrying costs are high.

I used 100% financing at a blended interest rate of 9%.

- $485,000 * .09 / 12 = $3,600 per month in interest.

- Plus another ~1,000 per month in taxes, insurance, utilities, etc.

My carrying costs here are $4,600 per month!

The earliest we’ll have access to the studio unit is 9/1/21. That’s if and only if the tenant agrees to leave amicably.

Let’s say it takes a month to do the work in both units. Then another 2 months to market and complete the sale. That puts us at an exit date of 11/30/2021. Let’s round up to the end of the year: 12/31/2021.

June 25 to December 31 is 6.25 months of carrying costs, or $30,000.

- +$650,000 sales price

- -$40,000 sales cost (6%)

- -$30,000 carrying cost

- -$30,000 improvement cost

- -$485,000 purchase price

- = $65,000 in potential net profit.

This math looks way too simple so let’s chop off another 15% and call it $50,000 in net profit.

My preferred route if we decide to sell is to do nothing and sell the property in as-is condition.

It’s not worth spending all that time and money to net the same profit.

🎯 Where Will We Land?

I’m excited to see how this all shakes out. This is the first property I’m buying where I’m more interested in flipping than I am holding. The main reason is there’s not a lot of equity here.

Definition: Equity = Value - Loan Balance.

I believe our equity today is $550K - $485K = $65K.

I could be wrong, but I think most people prefer to sell properties with a lot of equity so they can cash out. I am the opposite. I only want to sell if there’s not a lot of equity.

When there’s a lot of equity, I’d rather refinance the property, keep it, and ride it into the sunset.

Hear me out. If we sell this house for $550K today, the partnership will net ~$50K.

My share of that will be something like $35K pre-tax. Don’t get me wrong, $35K is a lot of money, but it’s not going to change much for how we live our lives today.

Now let’s say we spend $30K improving the property and we’re into it for $515K. Somehow we get an appraisal for $650K and we’re able to refinance 75% of that out. That’s enough to pay off almost all of my purchase money loan. (650 * 75% = 487.5).

Then I’d have ~$40K of cash left in the deal, but ~$160K of equity (650 value - 487.5 loan). I may or may not make a few hundred bucks per month over the life of the deal.

However, in 30 years, it will be paid off and it’ll be worth close to $900K if we assume just 1% appreciation per year.

Now THAT is life-changing money.