Livin' La Vida Luna

We went glamping at Chick-Fil-A last week. Luna filled up on fries 🍟 and nuggets 🍗 and barely made a dent in her carrots 🥕.

Think we may have messed up the order of operations on that one 😬.

It took me about 6 months to refinance my 4-family investment property.

I spent most of that time chasing loans I wouldn’t qualify for.

Then my cousin found me a lender that was willing to do a “no-doc loan” at a decent rate and term.

A “no-doc loan” requires very little, if any, documentation from the individual borrower. I didn’t have to submit recent pay stubs or 2 years of tax returns. They did, however, check my credit score.

Throughout the experience of talking to half a dozen different lenders, I realized everyone wants the same basic information.

At first, I was redownloading, reuploading, and resharing bits and pieces of information from a handful of different sources. Tracking those files down was a pain every time.

Then I found a better way.

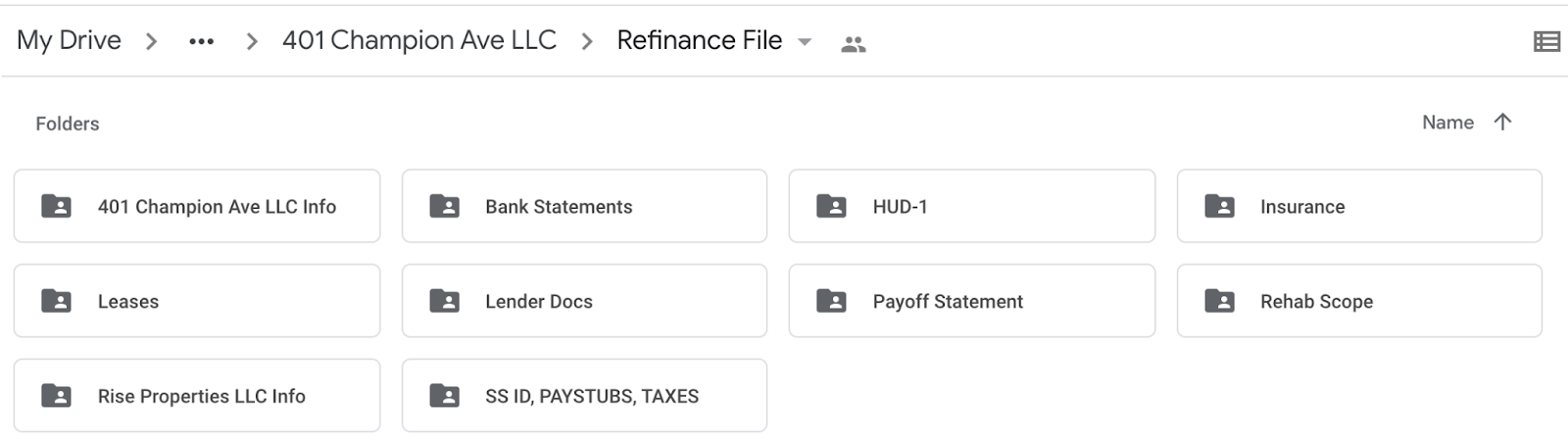

I made a new folder in my Google Drive and housed everything in one place.

I called it, “Refinance File”. Pretty original, right? 😉

In the rest of this post, I’m going to go through the entire file path so when you go for your next refinance you can be well prepared.

If you create this type of repository, all you have to do is share the link with your lender during the underwriting process and then unshare the link after closing the loan.

Folder 1 - LLC Specific Docs:

If you’re refinancing a property held in an LLC, you’ll need the following documents:

- Certificate of Formation

- Employer Identification Number

- Signed Operating Agreement

- Articles of Organization

The Certificate of Formation and Employer Identification Number documents are provided by the State in which you are incorporated. You should have these saved from when you opened your LLC.

If you do not have these documents, you can pay to download them off your state’s business website. You can do that here if your business is registered in New Jersey.

An Operating Agreement is a document that outlines the purpose of your business. It’s usually written by an attorney and signed by all members of an LLC.

If you do NOT have an operating agreement for your LLC, create one as soon as possible. If you’re in NJ and need a lawyer to write your operating agreement, reach out to Casey Eggers.

You only need to pay for an Operating Agreement once. After that, use it as a template and just change the names and dates assuming your business activity stays the same.

Articles of Organization are like the organization’s Bill of Rights. They define the rights, duties, and liabilities for each member of an LLC. They are produced with the Operating Agreement and sometimes can be included in the same document.

Folder 2 - Bank Statements:

Upload your last 3 months of bank statements.

Every time a new statement becomes available (monthly), upload it to this folder. Don’t wait for the lender to ask you for updated statements. Take initiative, be prepared.

If you are refinancing an investment property and it has a separate bank account, create 2 sub-folders.

One for your personal accounts and another for your rental property. Dia and I have 2 checking accounts so I had to create 3 sub-folders.

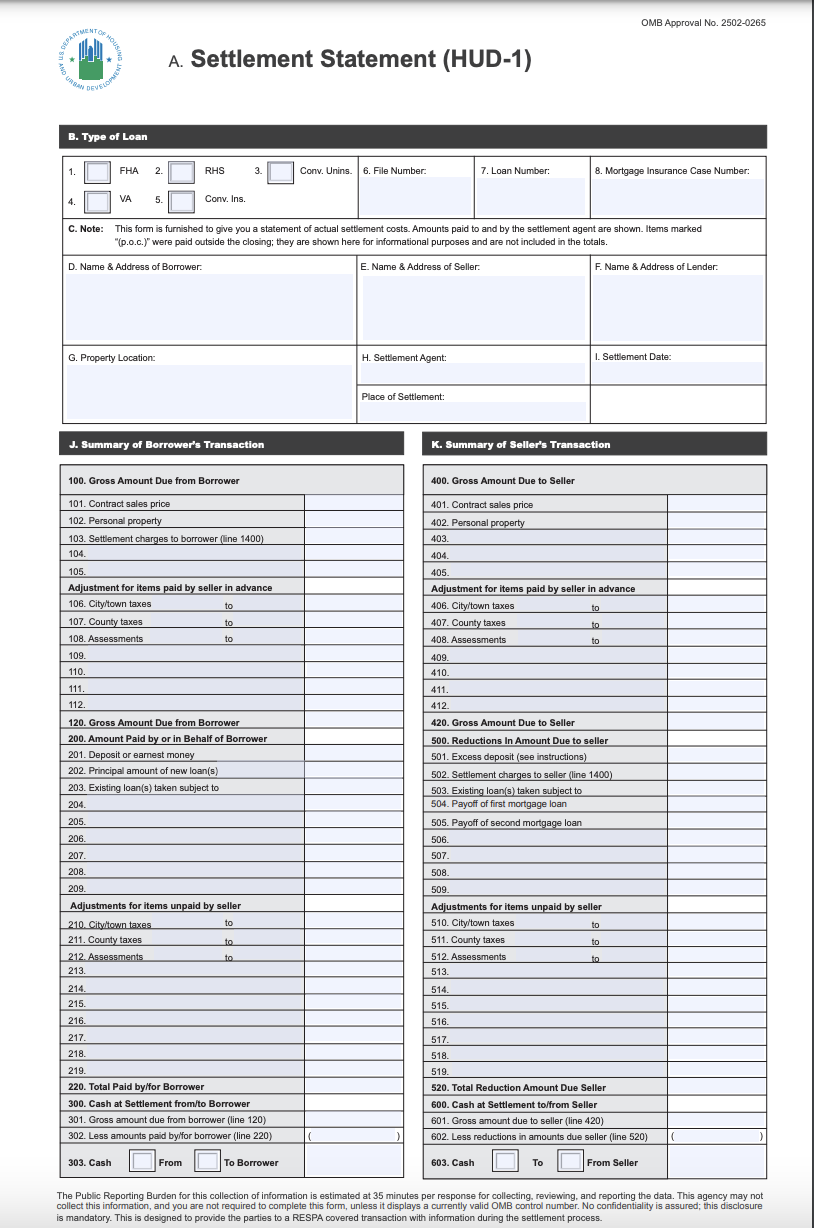

Folder 3 - HUD 1:

HUD (United States Department of Housing and Urban Development) statements are settlement details provided by Title Companies any time you have a capital event on a property (purchase, sale, refinance, supplemental loan).

It’s the document split into two columns: borrower and lender or buyer and seller.

If you are refinancing a property, the lender will likely want to see the HUD Statement from when you originally bought the property.

A sample HUD statement looks like this:

Folder 4 - Insurance:

The lender is going to ask for your insurance binder, or at least the declarations page.

They want to see:

- How much your monthly insurance premium is

- If you’re properly insured

- If you’re in a flood zone

- Who your current insured mortgagor is

If you don’t have your insurance binder, email your agent and ask for them to send you a soft copy.

If they push back, you might have to actually create an account with your insurance provider and download it off their portal.

Folder 5 - Leases:

If you’re trying to refinance an investment property, you will need SIGNED leases from your tenants.

The underwriter for the loan is going to compare the rental rate in your lease to the deposits in your bank account. If the deposits don’t match your rental rates, you’ll have some ‘splaining to do.

They are also going to check if your bank account minimum balance is AT LEAST the security deposit amounts you’re supposed to be holding.

Let’s say you have 4 units renting at $1,500 each, and according to your lease, each tenant gave you a $2,250 security deposit (1.5 months). You should have $9,000 ($2,250 *4) in the bank.

Folder 6 - Lender Docs:

This folder might need a better name. After all, everything we’re preparing is basically a “lender doc”.

Anyway, here’s where I upload miscellaneous items like:

- Appraisals

- Inspections

- Credit Reports

- Lender Conditions

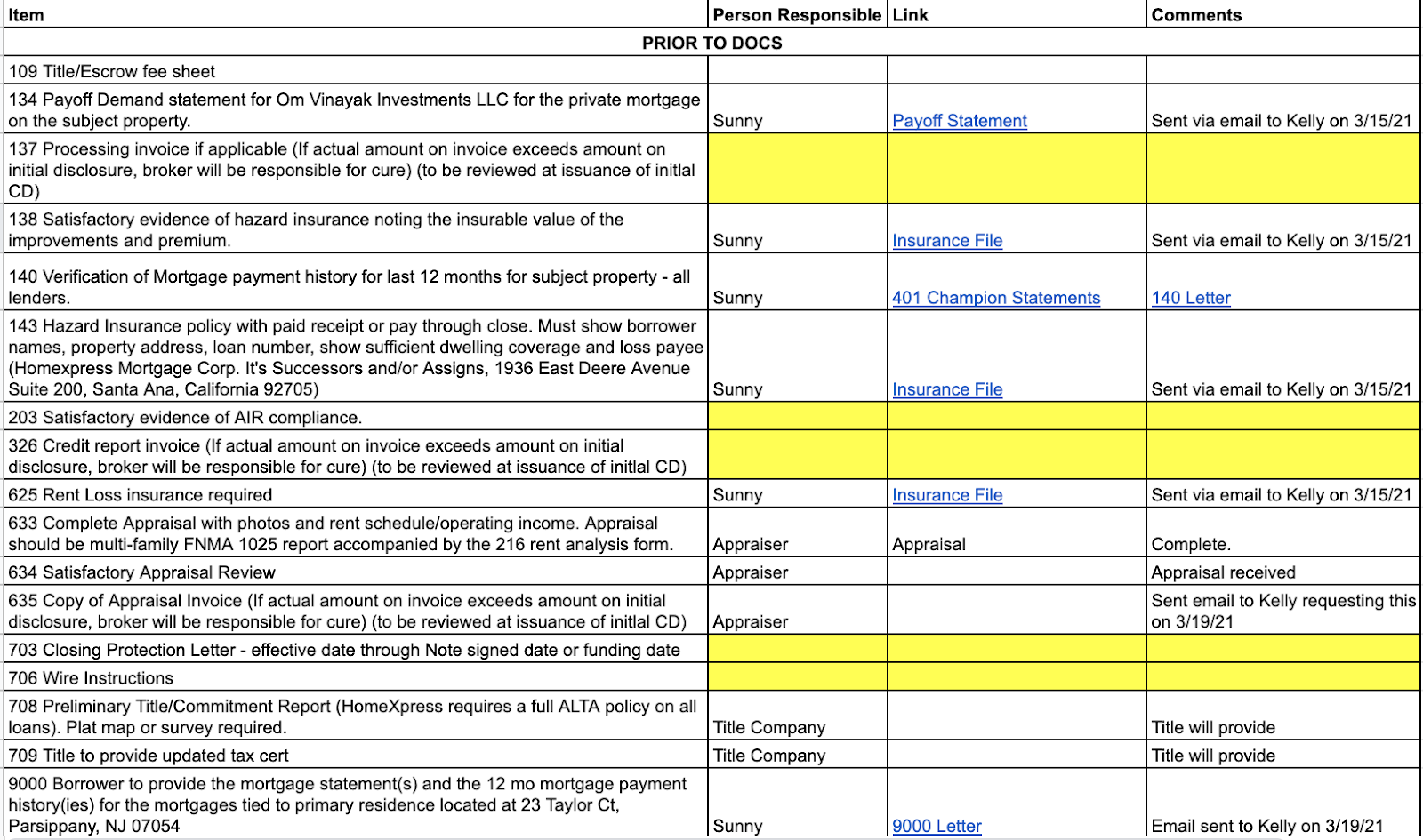

Lender Conditions is essentially a checklist of items the borrower needs to provide before the Lender can move forward with the loan.

Once they provide you with this list, upload it into an excel file with 4 columns.

- Condition

- Party Responsible

- Link

- Comments

Here’s what my lender conditions tracker looked like on my most recent finance:

Folder 7 - Payoff Statement:

If you have an existing mortgage on your property, you will have to reach out to your current lender to obtain a “Mortgage Payoff Statement”.

This document details how much your current lender needs to satisfy their loan.

I had a $408,000 private money loan against the property I was refinancing. My new lender was giving me a loan for $441,750.

Of the $441K in new money, the first $408K went to pay off my existing lender. If you don’t pay off your existing lender, they won’t discharge their mortgage. If they don’t discharge their mortgage, your new lender won’t lend to you.

It can take a lender up to a week or two to provide a payoff statement so plan accordingly.

Folder 8 - Rehab Scope:

Lenders want to know what kind of work has been done to the property.

This is the folder where you upload all your receipts for improvements made.

- Home Depot Receipts

- Contractor Receipts

- Appliance Package Receipts

- Landscaping Receipts

Every dollar you spent improving the property should be in this folder.

Why do they want to see this information? Let me explain using my specific example.

I bought my 4-family home for $240,000. One year later, it was worth $589,000. This wasn’t a case of insane appreciation in the market. We spent $160,000 bringing this property up to its highest and best use.

We also had $160,000 worth of receipts to prove it. So although we “only” spent $400,000, we achieved an equity value add of $189K.

If we couldn’t prove our renovation budget, I don’t think they would have bought our story.

Folder 9 - Partner Info:

I had a partner on this deal. This folder contained the same information on my partners as “Folder 1 - LLC Info” contained on me.

This folder is where I put my partners’ Certificate of Formation, EIN, Operating Agreement, & Articles of Organization.

If you don’t have partners, you won’t need this folder.

Folder 10 - ID, Paystubs, Taxes:

I didn’t end up needing this file for my no-doc lender, but it comes in handy anyway.

This is where I uploaded a picture of my driver’s license (front and back), my last 4 paystubs, and 2 years of tax returns.

If you have nothing to hide, act like it. If you do have something to hide, hide it and cross your fingers.

Good Luck!

Refinancing property feels more invasive than a colonoscopy. Sharing your intimate personal financial details with a stranger is a difficult task.

Remove the “pain” or “shame” by reducing the number of inbound requests you have to satisfy.

Otherwise, it’s death by a thousand cuts. You’ll get a new email every day asking for another document. It’ll seem endless.

Instead, take the approach I’ve outlined here. Get all your docs in a row. Upload them to a cloud drive and share that folder with your lender. Once the loan closes, take away their access and remove any sensitive files from the cloud.

Referrals:

If you need referrals for your refinancing needs in New Jersey, please try the following people:

- Attorney - Casey Eggers

- Mortgage Broker - Mehul Tamakuwala

- Insurance Agent - Sam Vij

- Banking - Francesca @ Chase Florham Park