Livin' La Vida Luna

Luna had two snow days off from school this past week. Keeping her entertained takes a Herculean effort.

I call this collage, "The 4 Stages of Hide-and-Seek"

My First Commercial Property

I’m under contract to buy property #3, which will bring me to 11 units total. We should be closing on or around 2/17/21.

This rental portfolio all started with the 4-family we bought back in January 2020. The initial goal was to buy an asset that produced enough cash flow to pay for Luna’s daycare in the short term and build up enough equity to pay for her college in the long term.

I didn’t expect that one deal to turn into 11 units across 3 properties in 13 months.

How We Found This Asset

The longer I’m in this business, the more I realize real estate investing is mainly a relationship game.

We were introduced to the seller by the owner of the 3-family home we bought in September 2020. We were introduced to the owner of the 3-family home by our contractor on our 4-family property.

These 3 deals are all connected. This is the law of the first deal in action.

The Asset:

Here are a few details of the property.

Location:

- Riverside, NJ

- 0.2 miles away from Light Rail (45 min to Center City, Phila)

- Downtown-like street with plenty of bars, restaurants, etc. nearby

Mixed-Use:

- Unit 1: 1,600 sf - Commercial Space

- Unit 2: 600 sf - 1 bed, 1 bath

- Unit 3: 960 sf - 2 bed, 1 bath

- Unit 4: 700 sf - 1 bed, 1 bath

- Garage: 960sf - 2.5 cars

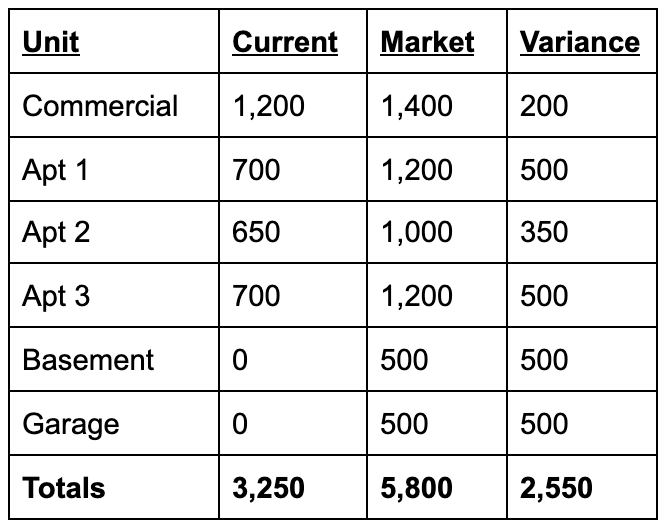

Current Rents vs. Market Rents:

We expect to increase the gross potential income on this property by a little over $2,500 per month. A 78% increase to existing rent roll.

We probably won’t capture all of that upside, but we will try to get close.

To stay conservative, we only underwrote to a $2,000 increase in the rent roll.

A little more on this later.

The Opportunity:

- Current rents for residential units are significantly below market value.

- Convert basement to storage units or another commercial space.

- Existing First Floor Commercial could be cut in half to create another residential unit.

- Garage sits on a 20x100 lot zoned for Single Family Residence (sell-off / develop)

Bid, Then Negotiate Terms

My partners and I made an offer of $310K after visiting the property and looking at the seller’s actual numbers. The seller wanted $350K.

My partners, who are also agents, offered to list the property at $350K and told him we would buy it in 90 days at $310K if it didn’t sell.

Surprise. It didn’t sell. We’re now under contract to purchase at $315K.

We didn’t just sit on our hands for 3 months.

In the span of those 90 days, we made a lot of progress on our business plan:

First, we helped the current owner rent out the garage at $500/mo. This was huge because we weren’t sure if this space could generate meaningful revenue.

Second, we extended the commercial space lease an extra year to August 2022 and increased their rent slightly.

Third, we asked the seller to carry a $100,000 note at 5% interest only for one year. This is called “seller financing”. It’s when the seller leaves some of their equity in the deal to reduce the cash out of pocket for the buyer.

ALWAYS ask for seller financing.

The seller currently uses the basement for storage. We asked if he was interested to continue using the space and he said yes. He signed a 1-year lease to rent the basement for storage for $400 per month.

The interest owed on his seller financing is $417 per month (100,000 * 5% / 12 = $417). So we only have to pay him $17 * 12 for his $100,000 loan.

Fourth, the seller agreed to deliver 2 of the 3 residential units vacant. One of the units needs some work, but the other is ready to go as-is. We tested the market on Facebook Marketplace and received a lot of inquiries.

We should have newly signed leases in place before close.

The seller also agreed to ask the 3rd residential unit to increase their rent from $700 to $900 before closing. If the tenant does not agree, we are asking that unit to be delivered vacant as well.

Finally, we asked for a 2 week inspection period. This property is in amazing shape, however, I always get an inspection done. It’s the fine details invisible to the naked eye that can cost an arm and a leg to fix.

In exchange for satisfying all our asks, the seller required us to escrow a deposit of 2.5% of the purchase price. We usually get away with 1% of the purchase price or less.

At this point, the only thing preventing us from closing is a wicked curveball from the inspection.

ProForma

Let’s work our way down from the top.

Revenue:

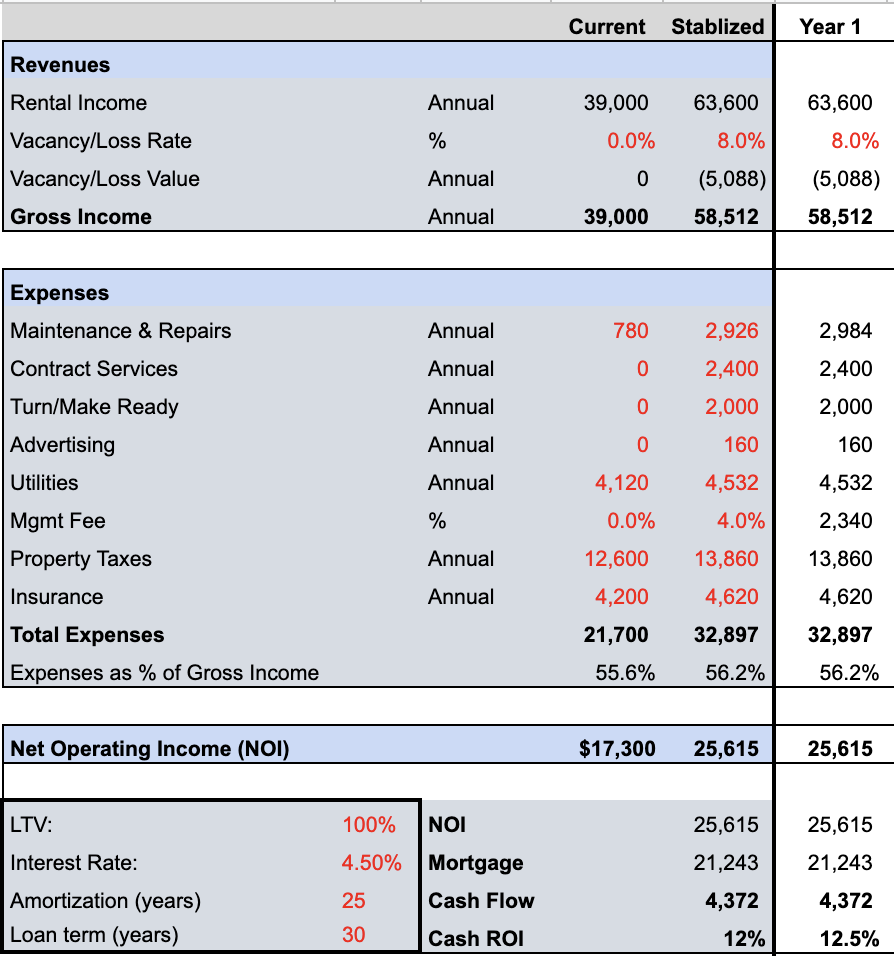

- Rental Income: We project a 24K increase in top-line income (2K/month)

- Vacancy: We always project 8%, which equates to 1 month per unit. (1 / 12 = 8%)

The rental income increase seems aggressive, but we’ve already locked in a $1,000 increase before close by renting out the garage ($500), the basement ($400), and increasing the commercial space rent ($100).

Expenses:

We used the seller’s actuals as the basis of our underwriting and added a few expense line items. We came in 10K (50%) higher than the seller’s expense numbers, which makes me feel like we’re being too conservative.

- Repairs & Maintenance is 5% of Gross Income at ~$250 per month.

- We added Contract Services (exterminator, landscaper) at $200 per month.

- We added Units Turns at $500 per unit per year.

- We added Advertising (on Zillow) at $10 per week per unit for 4 weeks each.

- We added a management fee as 4% of gross collected rents.

- We increased the utility actuals by 10%.

- We increased the current property taxes by 10%.

- We increased the current insurance by 10%.

Net Operating Income & Cash Flow:

Our NOI is projected to be $25K per year. We’re financing 100% of the purchase with short-term interest-only debt. The blended rate across all sources is 7%.

$315,000 * .07 = $22K per year. It’ll be tight, but there’s enough buffer in our numbers to satisfy the short term debt.

It will take ~6-8 months to get this property refinanced into long term debt. At which point, we will seek a full cash-out refinance of $315,000 at ~4.25% amortized over 25 years.

This will give us a debt service coverage ratio of 123%. Banks typically look for 125% minimum as the (DSCR), so one of a few things will have to happen.

- Our loan amount will need to decrease (hopefully not happening)

- Our loan terms will need to improve (probably happening)

- Our revenues will need to go up (probably not happening)

- Our expenses will need to go down (probably happening)

There are a lot of moving parts here. However, I think we’re in a good position to cash flow ~$5K per year here with little to none of our own money left in the deal.

Value-Add:

A mixed-use property is valued differently than residential property.

A residential property (1-4 units) is valued using the Comparable Sales Approach. CSA = An asset is worth what like-kind assets in the immediate vicinity recently sold for + material adjustments.

A commercial property (5+ units, commercial space), however, is valued by dividing the Net Operating Income by a Capitalization Rate, or Cap Rate for short.

A capitalization rate is the acceptable expected rate of return for an asset.

For a really stable asset like a newly constructed 300 unit apartment building with loads of amenities, the Cap Rate can be as low as 4% in today's market.

For a 12 unit run-down building in the wrong neighborhood, you might expect a Cap Rate as high as 12% or 15%.

The easy way to think about Cap Rate is the acceptable expected rate of return if you buy the property with cash. You are happy to accept less of a return from a better building in a good neighborhood than a run-down building in a bad neighborhood.

This property falls into the center of the residential/commercial Venn-diagram.

On one hand, it’s considered a commercial asset because of the first-floor commercial space.

On the other hand, it’s also available to residential buyers using an FHA backed loan.

FHA loan rules permit the purchase of properties between one and four units. For mixed-use property, commercially zoned residential property, or other non-traditional purchases, HUD 4000.1 states:

“The non-residential portion of the total floor area may not exceed 49 percent. Any non-residential use of the Property must be subordinate to its residential use, character and appearance.”

“Non-residential use may not impair the residential character or marketability of the Property. The non-residential use of the Property must be legally permitted and conform to current zoning requirements.”

Value As Commercial Asset:

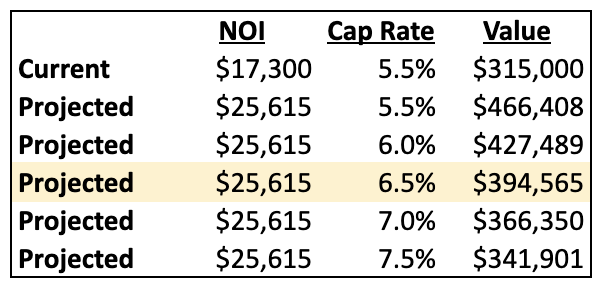

We’re buying this property for $315,000 and it currently has a Net Operating Income of $17,300. That computes a Cap Rate of 5.5% (17.3 / 315).

Our projected NOI is $25,615. If we take the same Cap Rate of 5.5%, that computes a value of $465K! (25.6 / 5.5%)

Personally, I do NOT think this asset justifies a 5.5% Cap Rate. If the market stays hot, I think it will fall somewhere between 6 and 7%. If the market cools off, I could see the value going as far down as a 7.5% Cap Rate.

*Cap Rates & Prices are inversely related. Lower Cap Rate = Higher Price.

Here’s the Cap Rate Sensitivity Analysis:

Value as Residential Asset:

We did not find a comparable sale for this property. There weren’t any mixed-use 4 unit buildings that traded hands in the past 12 months.

However, if we’re able to find an owner-occupant that uses an FHA backed loan to buy the property, we can back into the value by using the “Self Sufficiency Rental Income Eligibility” method.

According to Hud 4000.1, “Net Self-Sufficiency Rental Income is calculated by using the Appraiser’s estimate of fair market rent from all units, including the unit the Borrower chooses for occupancy, and subtracting the greater of the Appraiser’s estimate for vacancies and maintenance, or 25 percent of the fair market rent.”

So we know this property will rent for $4,400 without the garage or basement. We take out the garage because it’s on a different lot, and we take out the basement because it’s not legally recognized as an independent unit.

$4,400 x 12 = $52,800 in annual rental income.

If we take out 25% for vacancies and maintenance, that leaves us with $39,600 (52,800 * 75%).

If we take out property taxes, that leaves us with $25,740 (39,600 - 13,860).

If we take out insurance, that leaves us with $21,120 (25,740 - 4,620).

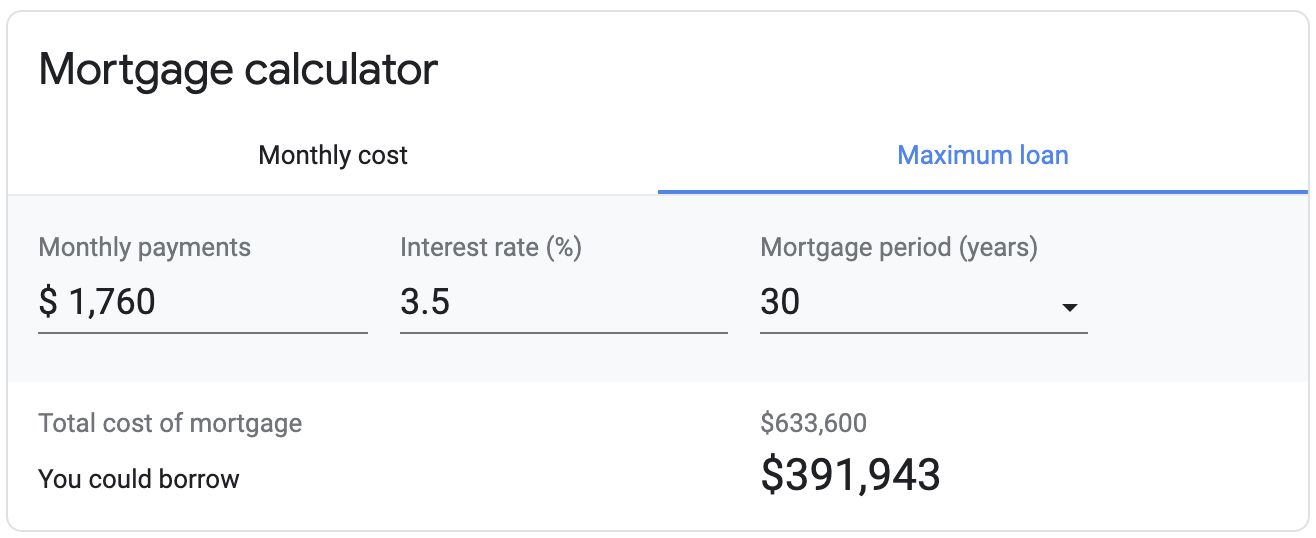

$21,120 divided by 12 is $1,760 per month available for principal and interest.

Using a reverse mortgage calculator, we can assume $1,760 per month at 3.5% over 30 years computes a purchase price of $391,943!

When It’s All Said & Done:

It’s going to take some work to get there, but we believe this property will be worth $390,000 - $420,000.

It’s not going to be immediate, however. There’s still a lot of work left to do.

We have $35K budgeted for renovations upon takeover. Then we have to find tenants at the market rate. Hopefully, we can identify these tenants before closing and schedule them to move in on 3/1/21.

We should be all in at $350K at the end of the day. If my underwriting is correct, we’ll create roughly $40 - $80K in equity and generate roughly $500 per month in cash flow.

Then it’ll be back to the drawing board.