Livin La Vida Luna

This chunky monkey just turned 9 months old. Nuts.

I Bought a 3-Unit Rental Property Without Ever Seeing it

In the Fall of 2018, I attended my first weekend-long Real Estate Investing Seminar. It was the Mid-Atlantic Summit hosted by Dave Van Horn in Philadelphia, PA.

One of the speakers, J. Scott, asked the audience a series of questions to kick-off his speech.

He asked...

“By a show of hands, how many of you have yet to do a single real estate investment deal?”

A little less than half the audience’s hands went up. He continued...

“Ok, Thank you. Now, by a show of hands, how many of you in this room have invested in at least 2 deals?”

Roughly half of the audience’s hand went up. He continued...

“Ok, now allow me to show you something incredibly interesting. By a show of hands, how many people here have invested in just ONE deal?”

Maybe 3 people, in a room of 100+ investors, raised their hands.

J. spent the next few minutes talking about something many real estate investors commonly refer to as the law of the first deal.

The law of the first deal states getting started is more valuable than waiting to get it perfectly right.

The odds are you won’t get rich off your first deal, but you will get something far more valuable than money: confidence & opportunity.

If you can manage to get over the hump of uncertainty, defeat analysis paralysis, and close on your first property... your second, third, and fourth deals practically fall into your lap and are typically much more lucrative.

The Law of The First Deal For Me

The law of the first deal played out for me in each of the separate categories of real estate investing I’m involved in.

After years of studying real estate, I made my first investment as a private money lender in December of 2016. I did my second private money loan in April 2017 and third in May 2017.

From Private Money Lending I shifted into investing as a Limited Partner in Large Multifamily Syndication. After months of studying that model, I made my first syndication investment in June 2017 and my second shortly after in December 2017.

After investing in dozens of Private Money Loans and Large Multifamily Syndications, I layered on a strategy of buying Small Multifamily rentals. I closed on my first 4-Family home in January of 2020. Then in September 2020, I closed on a 3-family property without ever seeing it.

How We Found The Property

Our General Contractor on the 4-family introduced us to the seller of the 3-family.

The seller of the 3-family was about to list his property on the market for $250K. One of his tenants had just moved out. He renovated the unit and wanted to sell it to an owner-occupant who would ultimately house-hack (live in one unit while renting out the other two to subsidize their cost of living).

The seller’s plan was good. Until we showed up. We made an offer for $215K (cash) and told him we could close in 30 days or less. He saw the merit in our offer and accepted it almost immediately.

Trustworthy Team

To be a passive investor and do well in this business, you need a team you can trust.

The basic team is made up of your Core 4:

- Deal Finder

- Property Manager

- Contractor

- Lender

I’m fortunate my partners on these small multifamily deals fill 2 of those roles (deal finder & property manager) and have preferred vendors for the other 2 (contractor & lender).

Once we had the property under contract, we ran an inspection to see what kind of shape it was in. We hired the same inspector we used on the 4-family. Once the report came back, we sent it to our contractor.

Some work had to be done, but nothing that scared us away. Our contractor assured us all of the work could be done within the allotted budget ($35K).

Analysis & Due Diligence

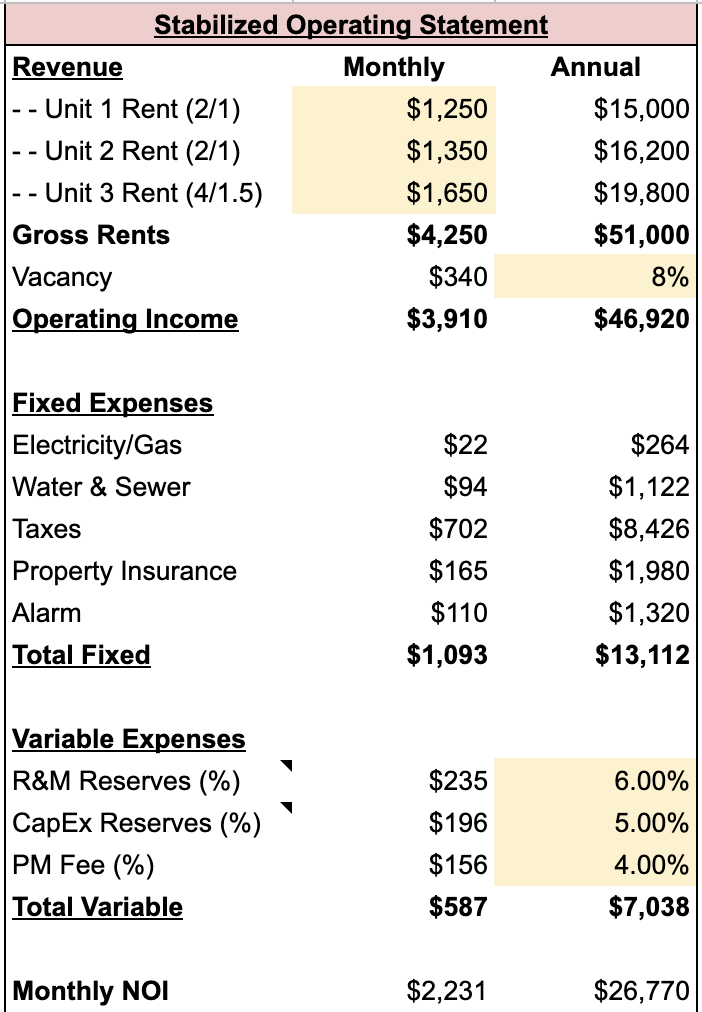

Once we knew our cost basis (purchase price & repair estimate), we moved on to our gross potential revenue.

This is a 3 unit home. Imagine an box. Draw a line down the middle. The left side of the building has two units (up & down) that are 2 bedrooms, 1 bathroom each. The right side of the building is one big unit with 3 bedrooms, 1.5 bathrooms, and a den.

The vacant and recently renovated 2 bed, 1 bath unit was on the top left. We expected it to rent for $1,200 per month. We ended up signing a lease before we closed on the property for $1,350. The tenant’s move-in date was scheduled for 9/1/2020, and we closed on 8/31/2020.

We inherited tenants in both of the other units. The 2 bed, 1 bath on the bottom left is paying $950 per month and the 3 bed, 1.5 baths on the right side of the building is paying $1,400. Both of these rents are significantly under market value.

If these tenants decide to leave after their lease term is up, we will improve the units and increase the rents to market rate, which would be ~$1,250 and $1,650, respectively. That’s a $550 increase in revenue per month.

Spending $35,00 to generate $550 per month is an 19% return on investment (550 * 12 / 35,000).

For our expenses, we took the seller’s actuals and increased them by 10%. For our variable costs like repairs & maintenance, capital expenditures, and property management, we forecasted ~15% of operating income. We underwrote vacancies to 8% (each unit empty for 1 month per year).

Here’s what the Pro-forma looks like.

Our net operating income per month lands a little over $2,200. However, this does not include debt service.

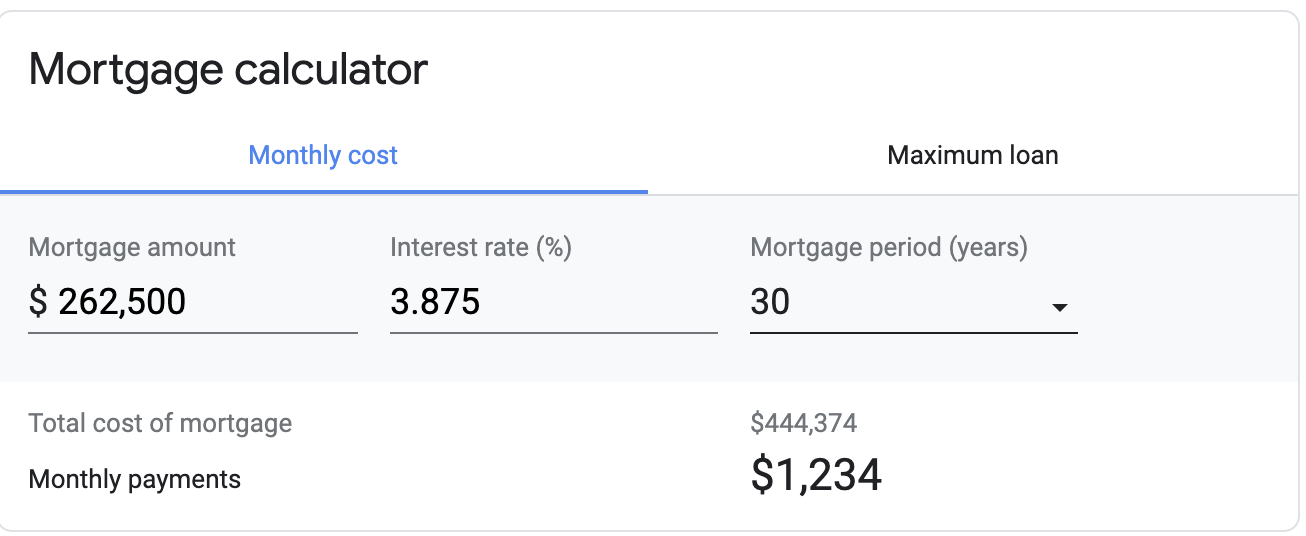

Right now, we are paying almost $1,800 per month in interest only ($215,000 * 10% / 12).

Once our inherited tenants leave and we spend the $35K to renovate the other 2 units, our interest-only payment will jump to $2,100 ($250,000 * 10% / 12).

At that point, we will seek a rate & term refinance into long term amortized debt. We believe this property will appraise for $350,000, which means we can get a loan for $262,500 at a 75% Loan To Value Ratio ($350,000 * 75%).

That extra $12,500 ($262,500 - $250,000) will likely cover closing closts.

$262,500 at 3.875% over 30 years computes to a monthly payment of $1,234.

So if we go back and take our net operating income ($2,231) and subtract out our new monthly mortgage payment ($1,234), our monthly cash flow will be $997. A thousand bucks per month with no money left in the deal. Amazing.

Opportunity & Confidence

This opportunity came as a direct result of my first deal in this space. If I never bought that 4-family, I would not have met that contractor. If I did not meet that contractor, he would not have introduced me to the seller of this 3-family.

This is the law of the first deal in action. Once you cross the chasm between tire-kicker and actual investor, things begin to change in your favor.

Would the seller have accepted an offer of $215K from a buyer who hadn’t closed on their first deal yet? I would argue no. I think he’d rather take his chances listing his property on the market than take a $35K haircut and risk the buyer not closing.

We presented a competitive offer backed by confidence. We didn’t even put a deposit down. We just signed a contract, agreed to a closing date and showed up on time.

It’s only a matter of time before the next homerun deal falls into our lap.