Livin' La Vida Luna

Luna started going to Daycare this past week. It's been a tough transition for all of us. Luna's resisting the bottle. Mom's worried. Dad just misses his little girl.

This is what she wore on her first day of "school".

I'm not crying, you're crying. 😢

Just Death, No Taxes

The New York Times finally got a hold of Donald Trump’s tax returns for the past 2 decades.

Aside from the audits, hundreds of millions of dollars in personally guaranteed loans coming due, and illicit write off activity, it seems most people are focusing on one thing: income taxes paid, or lack thereof.

According to the Times’ findings, Donald Trump paid $750 in Federal Income Taxes the year he won the presidency, and another $750 his first year in office.

This guy’s a multi-billionaire but somehow spends less money on his annual income tax than I spend on cereal.

Trump’s team obviously described the Times article as inaccurate.

I don’t know what the truth is. I’m not here to judge. Nor am I here to sway your political affiliation.

I just want to try explaining how the Tax Code set forth by the United State Government rewards business owners and real estate investors.

6 Tax Deferment / Avoidance Strategies I Use

I’m just getting started in my business and real estate investment career so I’m still playing kiddie games in the elementary school sandbox.

I learned and implemented the strategies I’m about to describe by visiting blogs, watching YouTube videos, listening to podcasts, and reading books on real estate investing.

I’m sure there are a lot more tricks of the trade I haven’t discovered yet, but I’ll get there.

1. Solo 401K / SEP IRA

Unlike a regular 401(k) plan, a Solo 401(k) retirement plan can be implemented only by self-employed individuals or small business owners with no other full-time employees.

I opened a SEP IRA, since I’m self-employed and have no full-time employees.

How is a Solo 401(k) / SEP IRA different than a traditional 401(k)?

In two major ways:

- The contribution limit is much higher. In a traditional 401(k), you can only contribute up to $19,500 per year (as of 2020). For a Solo 401(k) / SEP IRA, you can contribute up to 25% of your income, or $57,000, whichever is higher.

- You can set up a “self directed” account and put your contributions in there. A “self directed” account lets you invest in alternative assets like real estate, art, physical precious metals. Traditional 401(k) accounts are typically limited to investing in the stock market.

2. Depreciation

Depreciation is a real estate investors secret weapon. If you buy right, finance right, and manage right, you should be able to have tax free cash flow thanks to depreciation.

Let me explain how it works by using a 4-family home I bought in January 2020 as an example.

We bought the house for $240K. We put $120K into it to fix it up. So our cost basis is $360K.

Residential Real Estate Investments are depreciated over 27.5 years. However, you can only depreciate the building and improvements, not the land itself.

According to my property tax bill, the land is worth $110K, so I can only depreciate $250K.

- $360K cost basis - $110K land value = $250K

That brings my annual straight-line depreciation expense to $9,100.

- $250K / 27.5 years = $9,100/year.

We’re expecting this property to generate a positive cash flow of $1,000 per month.

Instead of paying income taxes on $12,000 per year, we’ll only have to pay income taxes on $2,900 / year.

- $12,000 - $9,100 = $2,900

That’s a tax savings of 76%.

- $9,100 / $12,000 - 76%

3. Cost Segregation Study + Bonus Depreciation:

The straight line depreciation scenario I described above is suited for mom and pop investors.

- When you depreciate a residential rental property, it’s over 27.5 years.

- When you depreciate a commercial rental property, it’s over 39 years.

Cost Segregation Studies + Bonus Depreciation are how syndication / private equity / institutional sized players juice up returns for their investors.

A Cost-Seg Study is performed by an engineer. They take inventory of all the individual components that make up a larger asset (think 200 unit apartment building) and assign a useful life to each component.

A basic list could look like this:

- Outlet Covers - 10 per unit - 5 year life - $2/unit

- LVT Flooring - 800 sq ft per unit - 10 year life - $3/unit

- Light Bulbs - 6 per unit - 5 year life - $5/unit

- Bathtub - 1 per unit - 5 year life - $250/unit

- ...you get the picture

After the engineer creates the itemized list of all the components that make up the building, a CPA will help identify which items have a useful life of less than 20 years.

Anything that has a useful life of less than 20 years can be depreciated 100% in year one!

What does this mean?

It means you’re likely going to have a negative tax return for that asset because depreciation expense will likely exceed the positive cash flow earned.

Why is a negative return a good thing?

A negative tax return for one asset can carry over and negate income you made elsewhere.

If you’re not a real estate professional, the passive losses get phased out after you earn a certain income, but if you are a real estate professional, you can take advantage of unlimited passive losses.

4. Real Estate Professional Status

Acquiring Real Estate Professional Status on your tax return is the ultimate cheat code to paying nothing in taxes.

Down, Down-Forward, Forward + Punch

So how do you do it? Two steps:

- Spend 750 hours per year (15 hours per week) as a “material participant” in a real estate business.

- You must spend 51% of your time in a real estate business.

The good news is, if you’re married, only one spouse has to qualify as a real estate professional for both parties to take advantage.

This is why you see so many highly paid professionals (doctors, lawyers, etc.) with a spouse that does real estate part time.

The couple can use the high income earned by one spouse to invest in real estate, then the real estate professional status by the other spouse to take full advantage of passive losses and avoid paying taxes on the income earned.

To obtain Real Estate Professional Status, you don’t need to be professionally licensed as a realtor, developer, broker, etc.

Your involvement can be rather broad:

- Acquisitions

- Sales

- Construction or Remodeling

- Conversions

- Operations or Management

- Rental or Lease Activity

5. Capital Gains Tax Avoidance

There are a few ways to avoid or defer paying capital gains tax.

The first way is with your primary residence. If you live in your primary residence for two of the last five years, you can avoid paying up to $250K in capital gains tax if you’re single and up to $500K if you’re married.

The second way is by doing what’s called a 1031 exchange on investment property. When you sell an investment property, you have to pay taxes on the capital gains (difference in sale price and purchase price + improvements) and also on the depreciation you took. You can avoid paying taxes on both by simply selling one asset and consecutively buying another, larger asset.

*There are certain rules you have to abide by to perfectly execute a 1031 exchange. I’m not going to dive into those here, but you can click here to learn what they are.

The third way to avoid capital gains tax on basically anything from stocks to real estate is through a qualified opportunity zone. A QOZ is an economically distressed community where new investments, under certain conditions, may be eligible for preferential tax treatment.

*There are certain rules you have to abide by to defer Capital Gains by investing in a QOZ. I’m not going to dive into those here, but you can click here to learn what they are.

6. Cash Out Refinance or Second Mortgages

When I was young(er) and dumb(er), I would advise my dad to sell his commercial property so he could buy something bigger and better that required less of his time.

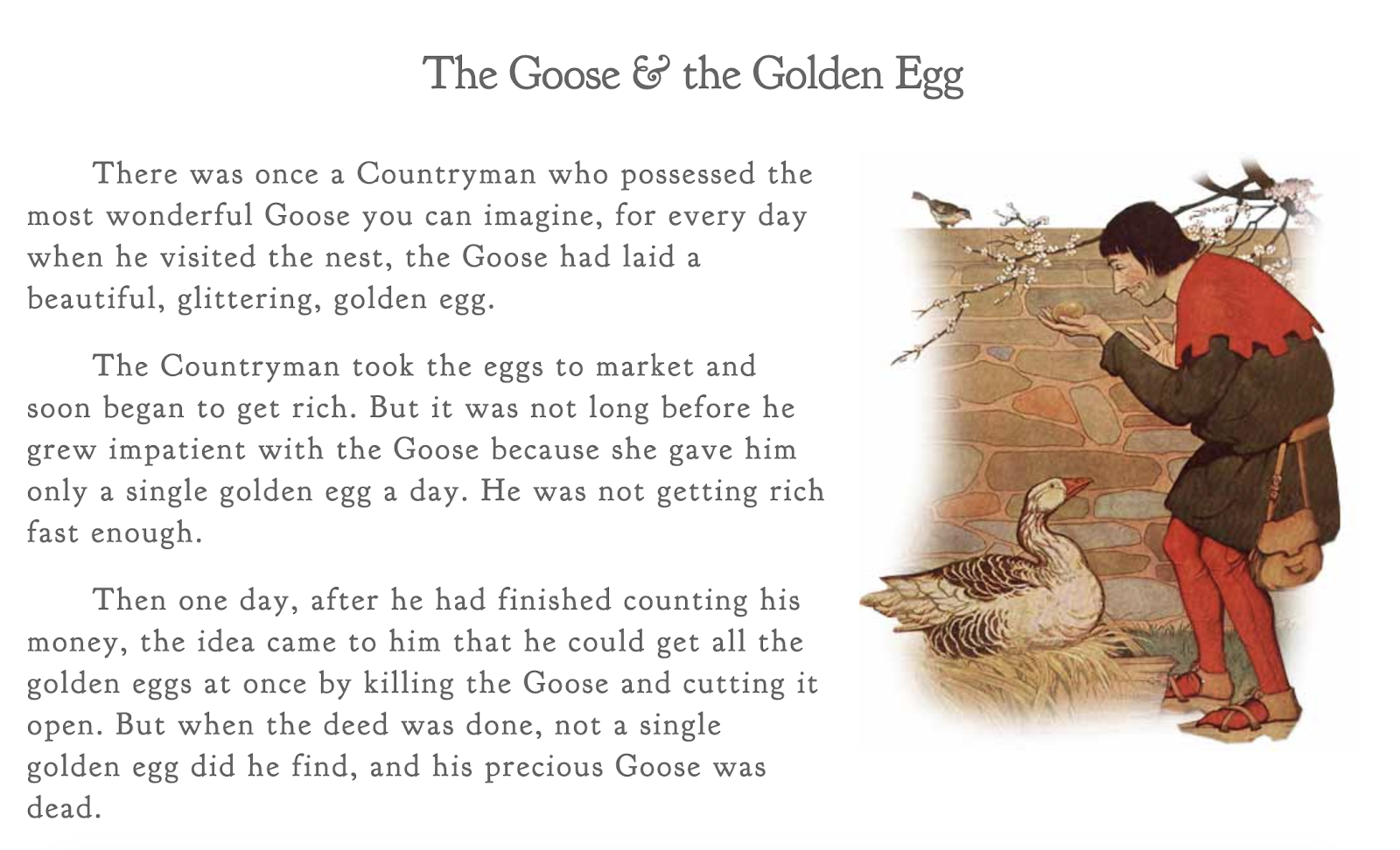

Then he would invariably tell me the story of the Goose That Laid The Golden Eggs.

If you haven’t heard the story, it’s a good one, so I’ll retell it here.

My dad’s commercial property is his Golden Goose. He’s owned it since the mid-80’s and has zero intention of ever selling it.

It’s completely depreciated down to zero. If anything, it’s a tax burden on him.

However, the one thing my dad’s commercial property has going for it is steady appreciation (through inflation mostly). Every 5 - 7 years, my dad refinances the property and pulls a chunk of money out for himself.

Sometimes he uses the money to make substantial improvements to the property. Other times he uses it to pay for 3 college educations in the span of 10 years.

Once you buy a property (with pre or post tax monies), you can refinance it or add a second mortgage to it and the proceeds from that capital event are tax free.

So let’s say you buy a $100,000 property with $20,000 (20%) down. In 5 years it appreciates to $125,000, and in the same time you pay down $15,000 of mortgage principal.

You can now refinance at a value of 80% of $125K, which is $100K. That new loan of $100K will pay off your old loan of $65K (80K - 15K), and you’ll be able to keep $35K in your pocket tax free (100K - 65K).

Now imagine doing that with a $1,000,000 property. Or a $10,000,000 property. Or in Trump’s case, a $100,000,000 property.

Just Death, No Taxes

The government has opened up tax loopholes to encourage all taxpayers to consider starting a business or investing in real estate.

Whether you decide to take advantage of them or not is up to you.

Now that I basically figured out how to pay close to nothing in income taxes, I can shift my focus to trying to live forever.