RIP to Chadwick Boseman.

Wakanda Forever. 😢

Livin' La Vida Luna

Luna is showing signs of rolling so we can't keep her in a swaddle anymore.

We tried a weighted sleep sack, but her startle reflex is way too strong. She freaks out because she has no idea what to do with her hands.

The current solution: Baby Merlin's Magic Sleep Suit.

This thing is so freaking cute and it makes me hungry for s'mores because my baby looks and feels like a gigantic marshmallow.

3 Real Estate Investing Rules of Thumb

When it comes to buying residential rental real estate, there are 3 “Rules of Thumb” investors keep in their back pocket.

These 3 guidelines are meant to serve as a checklist and are by no means enough to make a final decision on whether an opportunity is lucrative or not.

At the same time, an investor often relies on these 3 Rules of Thumb to avoid wasting time on analyzing a deal that probably won’t pencil out.

Here they are:

- The 70% Rule

- The 50% Rule

- The 2% Rule

Allow me to elaborate by telling the story about a 3-Family property we are acquiring on 9/1/2020.

- The 70% Rule

When buying rental property, investors try not to pay more than 70% of an asset’s After Repair Value (ARV).

Why 70% specifically? Because that’s what banks are typically willing to lend on non-primary homes (investment property, vacation homes, etc.).

The most savvy investors often pick up property with little to none of their own money.

How does this work?

A few months ago I was presented with the opportunity to buy a Triplex (3-Unit) rental property.

After looking at the comparable sales, I was semi-confident its After Repair Value could be in the range of $275K - $300K.

Nearby duplexes (2-units) sold for $205K - $250K. We can reasonably assume a single unit in a residential multifamily home (2-4 Units) in this market is worth $100K - $125K.

Based on an ARV of $275K - $300K, I’d be looking to offer somewhere in the range of $190K - $210K.

- $275K x 70% = $190K

- $300K x 70% = $210K

The asking price was $215K. It was an off-market deal we came to learn about from our contractor on another project so we did NOT negotiate the price. We simply put it under contract and ran inspections.

During the inspection process, we found most of the mechanicals (HVAC, Water Heater, etc.), and major CapEx (Roof, Windows, Flooring, etc.) had significant useful life left.

However, there were some electrical issues that required immediate attention. We asked our Contractor to take a look and he quoted us $7K to make the necessary repairs.

We went back to the seller and asked for a $7K concession at closing. Our purchase price remained $215K, but the seller would only take home $208K. The other $7K would go towards closing costs (Title, Taxes, Legal, Doc Fees, etc.)

We are buying this property with a short term private money loan that will fund 100% of the purchase price.

We need to let the transaction season for 6 months. In that time, we will make the necessary repairs to add value to the property.

After 6 months, we will go to the local bank and seek a refinance. If the property appraises for $275K, we will receive a new loan for $190K. We will use that money to pay our short term private money loan off, and also contribute $25K of our own dollars to fund the balance.

This is better than if we had put 25% down on the original $215K. That would require us to come out of pocket with $53K. ($215 x 25%).

If all goes according to plan, we’ll have acquired the same property for $27K less out of pocket.

- The 50% Rule

If you add up all the expenses associated with operating a rental property, you’ll find it lands right around 50% of the rental income.

If it’s consistently lower, you’ll be accused of being a slumlord. If it’s consistently higher, you’ll be accused of being a frivolous spender.

Expenses are line items like:

- Vacancy*

- Property Management

- Repairs & Maintenance

- Capital Expenditures*

- Utilities

- Insurance

- Security

- Landscaping / Snow Removal

- Property Taxes*

- etc.

*Vacancy, Capital Expenditures, and Property Taxes aren’t really “expenses” in Generally Accepted Accounting Principles, but they are money out the door so I refer to them as expenses for the sake of simplicity.

You have to be careful when using the 50% rule.

If your rental income per month is a paltry $500, your ability to spend money on repairs and maintenance is a lot different than if your rental income is $2,500.

Far too often, people are buying pig properties in the midwest that rent for $500-$750 per month and then get caught with their pants down when a major mechanical item needs to get fixed.

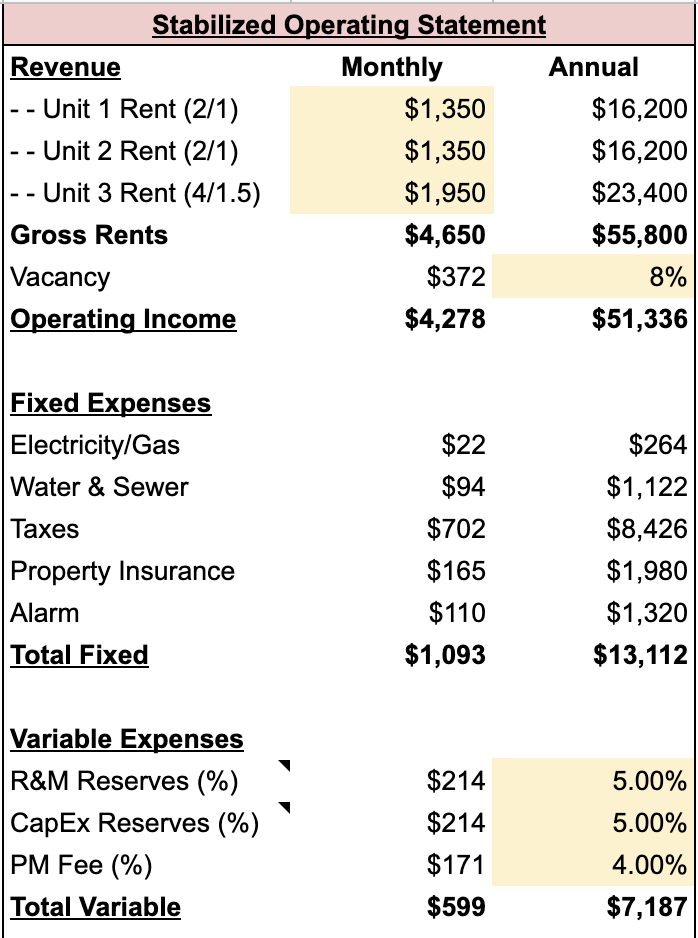

Here’s what our expenses look like for the 3-family home. This budget was made using the current owner’s financials. We increased all fixed expenses by 10% and added all the variable expenses.

Well would you look at that:

- $1,093 + $599 + $372 = $2,064.

- $2,064 x 2 = $4,128

Operating Income (after Vacancy): $4,278.

Coincidence? I think not.

Our reserve account balance for this property will sit at $7,500. That’s two years of Repairs & Maintenance and Capital Expenditure Reserves. We’ll be in great shape as things begin to go out of service.

- The 2% Rule

The 2% rule is the holy grail.

When buying rental property, investors are looking for their gross monthly rental income to be 2% of the purchase price.

So in our case, we’re looking for $4,300. ($215,000 x .2%)

The current rent roll is as follows:

- Unit 1: 2 beds / 1 bath

- Unit 2: 2 beds/ 1 bath

- Unit 3: 4 beds / 1.5 bath

Unit 1 is empty. After the last tenant moved out, the seller renovated the unit and left it empty because he thought an owner-occupant might buy the property.

Unit 2 is occupied by a tenant paying $950 per month.

Unit 3 is occupied by a tenant paying $1,400 per month.

We were sure these rents were severely under market rate.

How can you get an idea about what market rental rates are?

I use the following tools to determine rents:

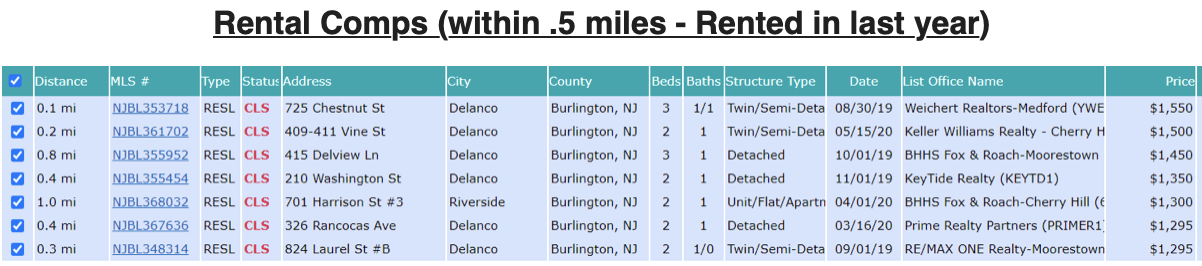

- MLS (Rental Comps Image Below)

- Zillow

- Craigslist

- Rentometer.com

The FIRST tool I use to determine potential rental income is HUD Fair Market Rents. This is the website that shows what the Section-8 Government Sponsored Program would be willing to pay in that market.

As you can see a 2 bed unit can rent for $1,340 and a 4 bed unit can rent for $1,920.

Before we decided to submit our non-refundable deposit, we put up a “ghost listing”. That’s a nice way of saying a fake listing.

We created a listing for the empty 2 bed unit at $1,200 per month. We were overwhelmed with applications. We knew we underpriced the market and ended up locking in a tenant for $1,350.

Now we know two things:

- Over time, we can raise the rent for the other 2 bed unit from $950 to $1,350.

- The 4 bed unit is currently at $1,400, but can probably achieve closer to $1,950.

$1,350 + $1,350 + $1,950 = $4,650 in Total Rents

$4,650 / $215,000 = 2.16%!!

Wrapping Up

As a real estate investor, I get bombarded with offering memorandums, off-market opportunities, stale MLS listings, etc.

I get a new “deal of a lifetime” email in my inbox almost every day.

I could not possibly fully analyze every single deal in detail. If I did, I’d be spending all my time in the spreadsheet and no time actually acquiring assets.

These 3 Rules of Thumb save me a bunch of time and headache.

I can quickly verify whether or not the asking price seems close to or under 70% of my expected After Repair Value. If it’s not, I pass.

I can quickly verify whether or not the rents are high enough for a 50% expense ratio to actually cover normal expenses. If they’re not, I pass.

I can quickly verify whether or not the expected rent will be 1-2% of the purchase price. If it’s not, I pass.

While I can’t automatically make a decision to do an investment if it meets these 3 rules, I can surely make a decision not to look further into an investment if it doesn’t meet any of the 3 rules.