The lease for our current apartment is up in December 2020. With the recent addition to our family, our current space is starting to feel a little cramped. Babies come with a lot of baggage!

We also have to start thinking about the added expense of day care once Dia goes back to work in a few months. The rent where we live takes up lion's share of our monthly nut.

In an attempt to get more space at a lower cost without sacrificing location, I've finally convinced Dia to entertain the idea of "house hacking" in a small multifamily property.

This week's post explains how I'm analyzing the first opportunity to present itself.

Click here if you want to read this weeks post in your web browser. Otherwise it's pasted below for your convenience.

Best,

Sunny

House Hacking Case Study

A real estate investment came across my desk and we’re highly considering purchasing it for personal use.

It also happens to make for a great long term investment.

In this post, I’ll take you through my thought process in evaluating the opportunity.

Opportunity Detail:

First, let’s start with what we know about the property now.

Deal Type: Off-market (not listed on MLS).

Subject Property: 2-Family Home in Montclair, NJ. 2,600 square feet.

- Unit 1: 2 beds / 1 bath

- Unit 2: 3 beds / 2 baths

- Garage: 3-Cars

Current Rent Roll: $3,450

- Unit 1: $1,550

- Unit 2: $1,900

- Garage: $0.00

Condition: Recently Renovated (< 10 years)

- Hardwood floors

- Stainless steel appliances

- Granite countertops

- Newer cabinets.

- Unfinished Basement (< 6’ ceiling)

Features:

- Central Air

- Washer / Dryer in each unit.

Immediate Work Required: None

Costs / Values:

- Purchase Price: $500,000

- Annual Taxes: $11,400 / year

- Insurance: $1,800 / year

FHA Backed First Time Home Buyer Loan:

Outright investment loans typically require putting 20-25% down. I’ve used these loans before to acquire properties in an LLC.

However, Dia and I have yet to buy a property in our personal names. Since we’re considering living in one unit and renting out the other, we can qualify for a primary residence loan backed by the FHA (Federal Housing Administration).

The FHA Loan appeals to first time home buyers for a few different reasons:

- Low Down Payment (3.5%)

- Low Credit Score Requirement (580)

- Down payment can come from savings, a gift from a family member, or a grant.

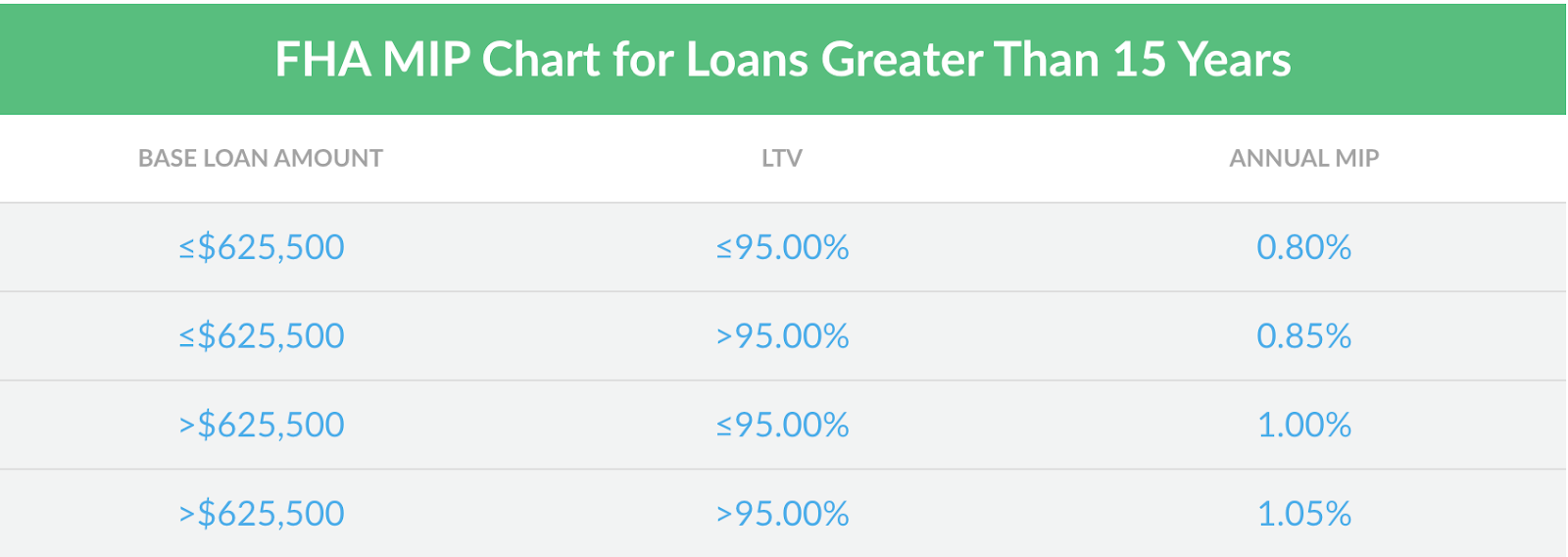

The downside to the FHA Loan is mortgage insurance.

Since the Loan To Value (LTV) Ratio is so high, lenders require the borrower to pay insurance in case they default on their payments.

That mortgage insurance is split into two cost components:

- An upfront fee (1.75% of loan amount)

- A monthly fee

The monthly fee sits on a sliding scale depending on base loan amount and LTV.

Source: LendingTree.com

I reached out to a mortgage broker and here’s the quote I received:

- Down Payment: 3.5% = $17,500

- Loan Amount: $483,500

- Term: 30 years

- Interest Rate: 2.875%

- Lender Fees: $0.00

- Upfront Mortgage Insurance Premium: $8,445. (1.75% of Loan Amount)

These terms compute to:

- Principal & Interest: $2,002 / month

- Mortgage Insurance: $345 / month (.85% of loan amount / 12)

Potential Upside:

Rental Income:

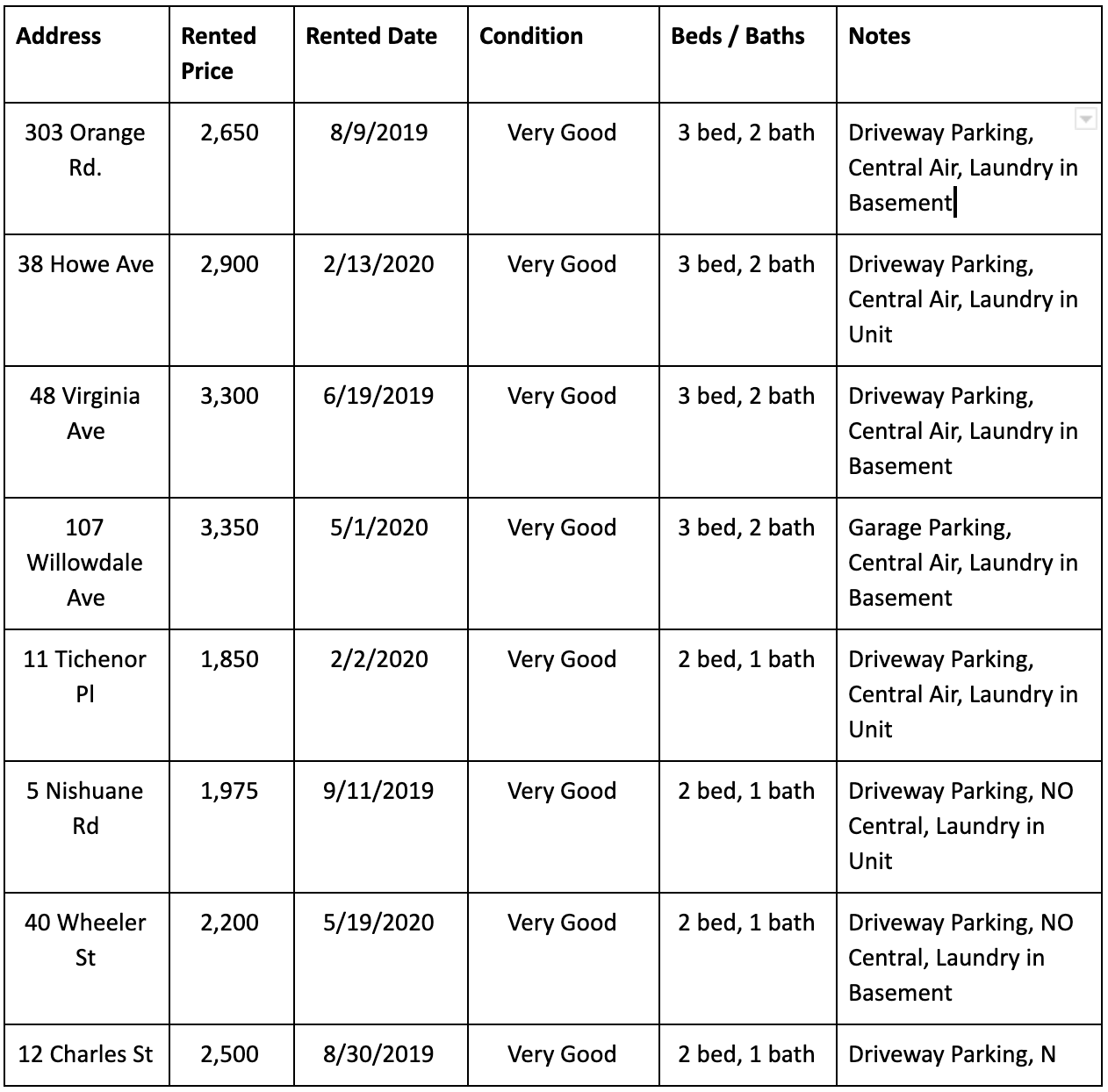

The current rents are below market rate. I use Rentometer.com to find market rate rents.

I also have comps from the MLS (<1mile from Subject, rented in past year) to support the market rate rent figures.

- 2 bed / 1 bath avg rent = $2,130

- 3 bed / 2 bath avg rent = $3,050

This is a $1,700 premium over what’s being paid by the existing tenants ($3,450).

For purposes of this exercise, I’m going to apply a 10% discount to the numbers above.

- 2 bed / 1 bath: $1,935 per month.

- 3 bed / 1 bath: $2,745 per month.

Equity Value:

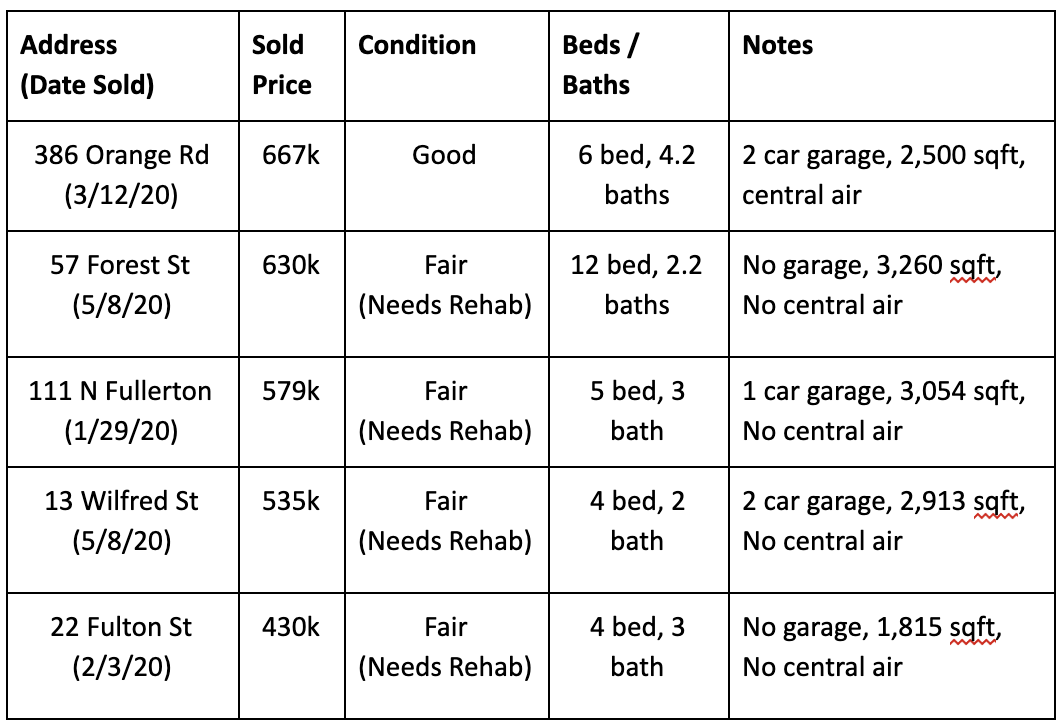

I typically use Zillow.com or Dealcheck.io to search for recently sold comps. In this instance, I have 2020 comps straight from the MLS.

The two best comps here are 386 Orange Road and 111 N Fullerton.

Orange road is 100 square feet smaller with, has 1 more bedroom, 1.5 more bathrooms, and 1 less car garage. It sold for $667K.

Fullerton has 400 more square feet, but no central air, 2 less garages, and a similar floor plan in terms of beds and baths. It sold for $579K.

The average of those two properties is $625K.

If I purchase at $500K and appraise for $625K, that’s an instant $125K in equity gained.

*mic-drop*

Running the Numbers (Pro-Forma):

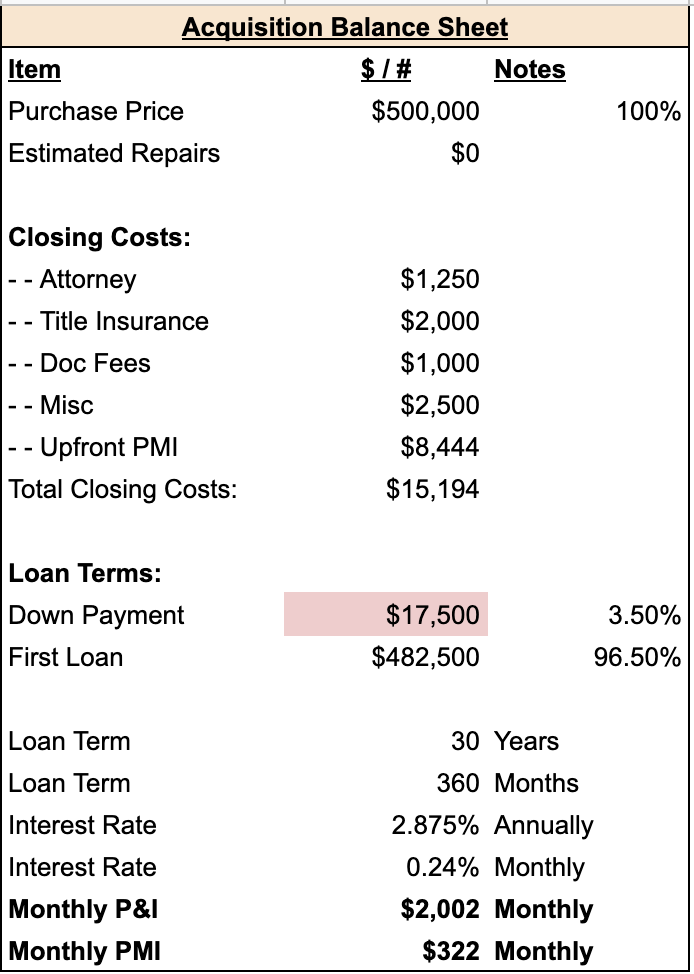

One of the biggest things investors fail to consider when evaluating a property is closing costs.

As you can see in the Acquisition Balance Sheet, I estimate $15K in closing costs, which is almost equal to the amount of the down payment, effectively doubling the cash required to close the deal.

When running the numbers, it’s more important to consider how the property is performing now vs. how it will perform at its highest and best.

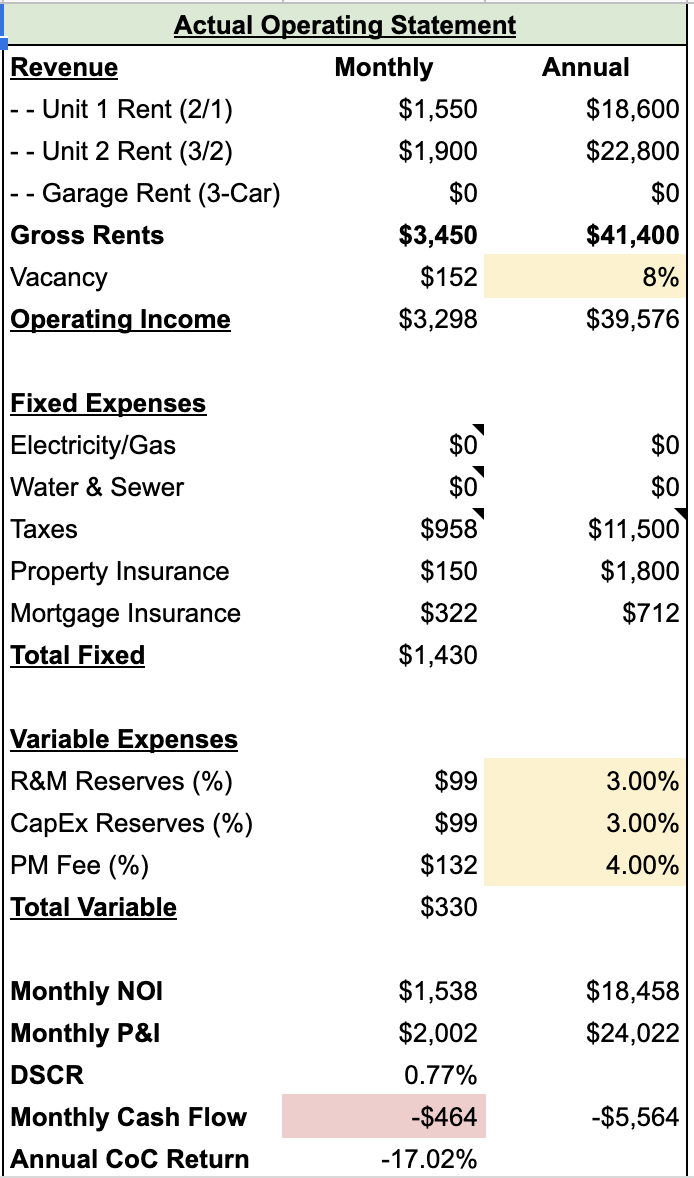

As you’ll see below in the Actual Operating Statement, if the rents stay the same, the property will lose $464 per month.

This loss includes preventative measures in the amount of $350.

- Vacancy - $150

- Repairs and Maintenance - $100

- Capital Expenditures - $100

The Actual Operating Statement also factors in $0 in revenue from the garage, which can typically rent for $50-$100 per space.

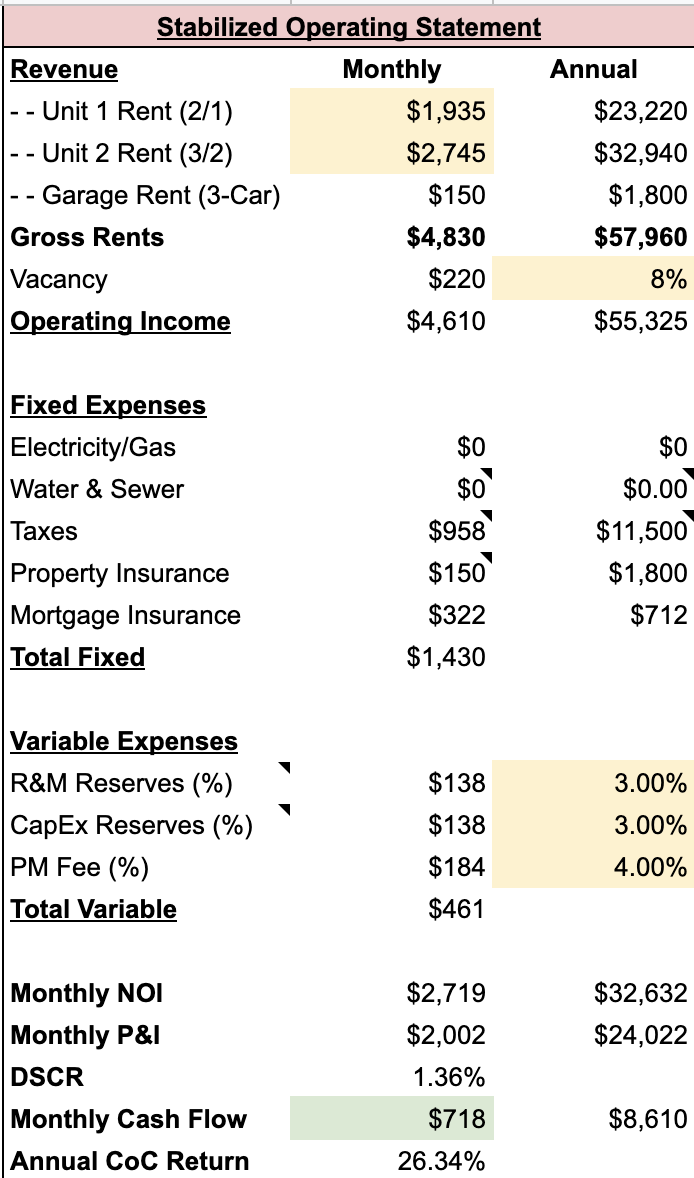

Now let’s look at this deal with our rose colored glasses and see what the Stabilized Operating Statement shows.

If we’re able to achieve 90% of comparable rents and lease the garage units at $50 per space, there’s $700+ in monthly cash flow to be gained.

That would be pretty sweet, but it’s a long road to that number. A lot of things have to go right to get there.

First, the current tenants have to leave without any fuss. Then, I have to find new tenants at market rate in the midst of a pandemic.

Finally, I have to either 1) upcharge the new tenants for garage spaces or 2) find someone random to lease out the garage and hope they don’t cook meth in there.

The real value in this deal is in the potential equity.

If this property actually appraises for $625K, it would be a bonehead move not to buy it at $500K today.

So that’s my next move. Order an independent third party appraisal (not from the lending bank) to see what this place is actually worth. That’ll cost me anywhere from $250 - $500.

Oh yeah, I would have to get an inspection done too.

House Hacking

I almost forgot to explain what this deal looks like if we use it as a primary residence.

House hacking is a great real estate investment strategy when owning multi-family rental properties. House hacking is when you live in one of the multiple units of your investment property as your primary residence, and have renters from the other units pay down your mortgage and expenses.

If we’re able to achieve market rents for the 3 bed / 2 bath unit and we decided to live in the 2 bed / 1 bath unit, we’d be paying $1,200 to live there.

- $750 positive cash flow minus 2BR rental income of $1,950

If we’re able to achieve market rents for the 2 bed / 1 bath unit and we decided to live in the 3 bed unit, we’d be paying $1,995 to live there.

- $750 positive cash flow minus 3BR rental income of $2,745

$1,200 for a 2/1 or $1,995 for a 3/2 is a steal in Montclair, NJ.

We’d live there for the minimum time required by the terms of our loan agreement and then move on to the next one.

--

Do you know someone who might be interested in reading this email? Feel Free to Forward it!

If someone forwarded you this email, you can sign up for my newsletter by clicking here.