In today’s real estate market (July 2021), sellers expect offers to come with as few contingencies as possible.

A contingency is a stipulation a buyer builds into their offer. These stipulations generally protect the buyer from losing their deposit in case they decide to back out of their purchase contract.

Some common contingencies buyers build into their offers are:

- Environmental (oil tanks, clean soil)

- Structural (roof, foundation, basement, walls, ceilings, and floors)

- Mechanical (HVAC, plumbing, and electrical)

Another honorable mention is the mortgage contingency. A mortgage contingency says the buyer is allowed to back out of a contract if they are unable to obtain financing.

Nowadays, putting a mortgage contingency into a contract is a sure-fire way to get laughed out of the room because it seems like everyone is buying in cash.

?What Does “Buying In Cash” Really Mean?

Before I started investing in real estate, I used to think buying a house “in cash” meant showing up to the closing table with a duffle bag full of $100 bills.

I watched way too many Rap Music Videos on 106 & Park when I was a kid.

After buying a handful of investment properties, I now realize buying a house in all cash simply means waiving your mortgage contingency when making an offer.

Making an all-cash offer doesn’t necessarily mean you CAN’T get a mortgage. It just means you won’t be getting your deposit back (typically 10% of the purchase price) if you can’t arrange for financing on or before the scheduled closing date.

?So Where Does all that Cash Come From?

Here are 4 common sources of funds when buying a house in “cash”.

1. Home Equity. The real estate market is about to enter year 15 of a bull run. The bottom of the last crash was in March 2007.

All the while, homeowners have been benefitting from paying down their loans and healthy appreciation, which ultimately creates a ton of home equity.

Unlocking that equity is as easy as:

- Cash-out refinancing at historically low rates

- Obtaining a Line of Credit against your property

I prefer a line of credit to a cash-out refinance, but I guess it depends on what you’re going to use the money for.

2. Business Equity. The latest recession caused by the COVID-19 pandemic was different than past economic downturns.

Government funding provided directly to businesses and consumers kept many entrepreneurs’ dreams alive and allowed many others to thrive.

Let’s pour one out for the business categories that depend on in-person transactions.

If your business survived the pandemic, I’d bet banks are willing to provide you a line of credit.

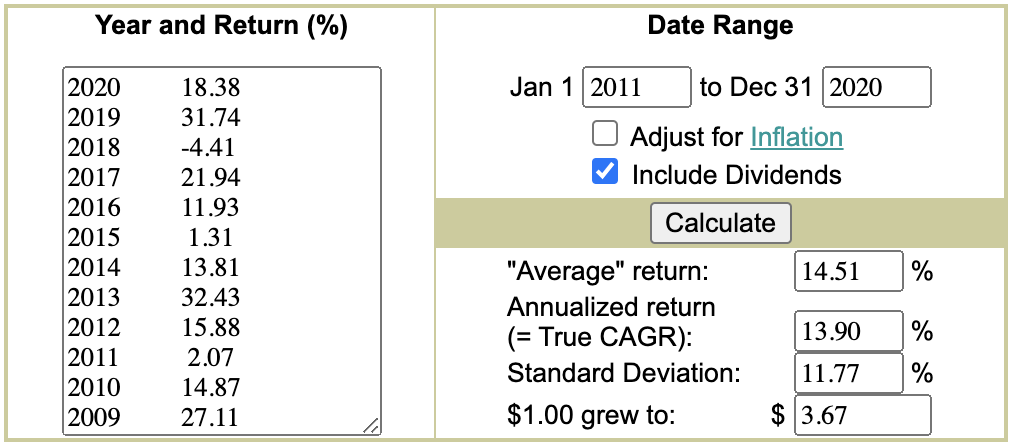

3. Equity in… Equities. The stock market has gone on an absolute tear over the past few years. The 10-year compound annual growth rate (CAGR) for the S&P 500 is ~14% per year.

If we apply “The Rule of 72”, that means an investor in the S&P 500 would have seen their money double twice in that same 10 year period. (72 / 14 = 5).

If you subscribe to /r/wallstreetbets, you might not be able to see past buying options on margin.

But if you’re a real estate investor or regular homebuyer with a sizable equities portfolio, you might be able to leverage that asset to buy a home in “cash”.

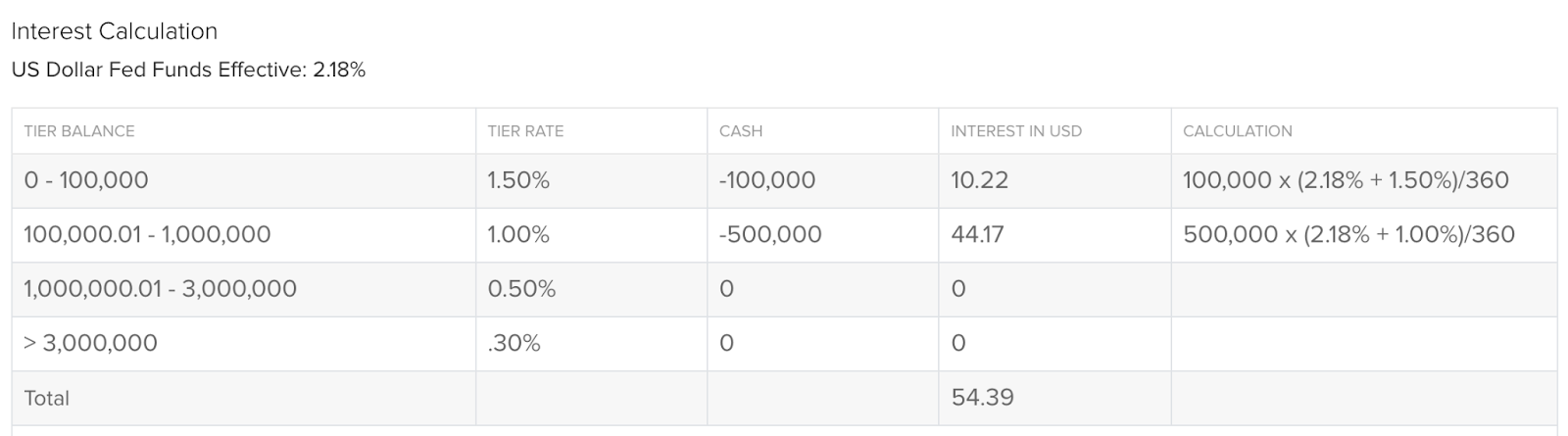

If your current brokerage or custodian doesn’t allow you to take loans against your stock portfolio, Interactive Brokers might.

Their rate is pretty good! The per diem interest cost on a $500,000 loan is only $44.17.

I typically pay anywhere from $110 – $165 per day for the same amount of money.

4. BOMAD (Bank of Mom and Dad). One of my favorite Blogs is Financial Samurai. Sam often spitefully writes about how many of his neighbors live in homes that were paid for by their parents.

LOL at that formula. I can’t wait to fund Luna’s down payment on her first home and turn her into a BOMAD stat.

4️⃣4 Reasons Why 100% Equity is Not Smart

Ok, now that we covered the 4 sources of funding a home purchase with “cash” or cash equivalents, let’s get into the 4 reasons why a cash purchase can backfire.

1. Asset Protection. This example is so cliche, but it paints a vivid picture so I’ll use it anyway. Imagine someone slips on ice and breaks their hip on your property.

If they lawyer up and decide to sue you, a loan against your property might be your knight in shining armor.

If their lawyer notices your property is free and clear of a mortgage, they’ll see nothing but dollar signs. All the lawyer has to do is sue the property owner for the value of the home and sit back and wait for a sale to occur.

If a lawyer sees that your property is encumbered with debt, they’ll likely pump the brakes.

2. Comingling or “Piercing the Corporate Veil”. Let’s say you fund the purchase of a secondary / investment home with money from an account tied to your personal name (checking account, stock account, etc.).

If you or the entity (LLC) that owns your secondary / investment property are sued, any good plaintiff attorney will argue your personal and business assets are comingled.

3. Higher Interest on Cash-Out Refinance.

There are two types of refinances:

- Cash-Out

- Rate and Term

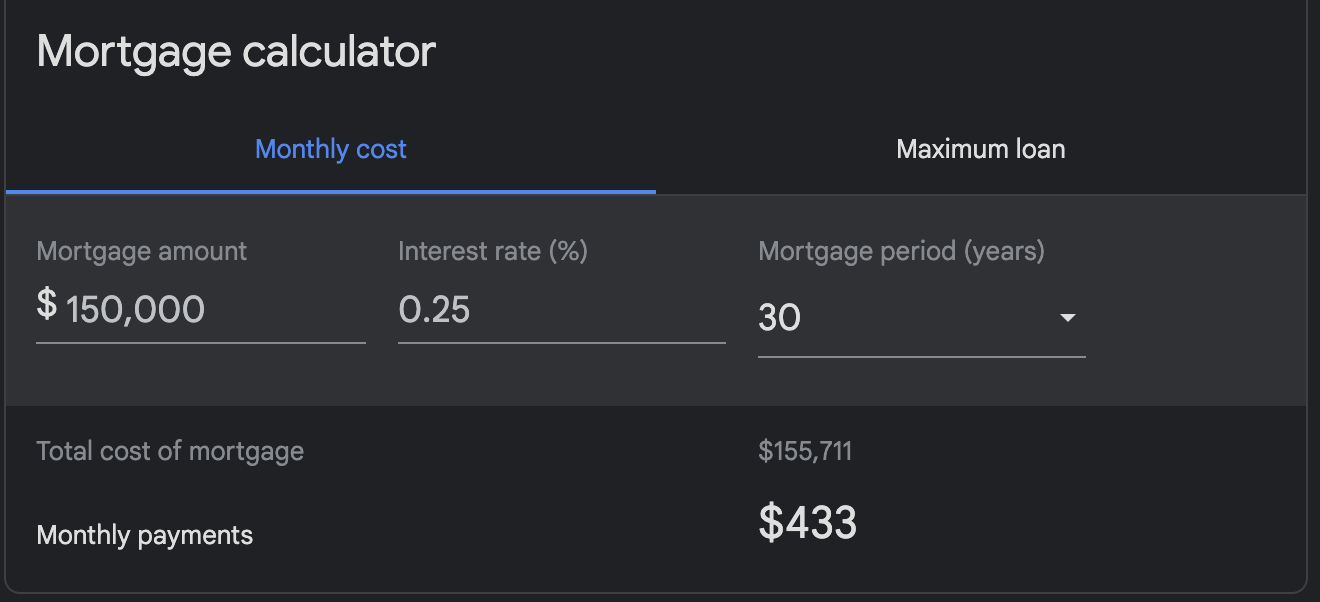

Let’s say you bought a home in 2010 for $100,000. You put down $25,000 and obtained a loan for $75,000 at 4% interest over 30 years.

Congratulations! Today, that home is worth $200,000 and you paid the loan down to $50,000. You have $150,000 worth of equity.

Provided you have the income to support it, most banks would be willing to lend you $150,000 against this property in a cash-out refinance (150 / 200 = 75% LTV).

Now you have 3 choices:

- Stay the course. Continue making payments on your existing loan and pay this home off in the next 20 years.

- Rate & Term refinance. Get a new mortgage at today’s lower rate but keep the loan amount $50,000.

- Cash-Out refinance. Go full send and take out a new loan for $150,000. Use $50,000 to pay off your existing loan and put $100,000 in your pocket.

Option 3 sounds awesome, but it comes at a price. When you cash-out refinance, you can expect the interest rate to be at least .25% higher than a rate and term refinance.

.25% doesn’t sound like much, but on a $150,000 loan over 30 years, .25% amounts to $5,711.

4. Marketers Galore. The final nail in the coffin of paying in cash is exposing yourself to tacky marketers that are on the hunt for a deal. How do I know this? Because I’m that guy, pal.

Every month, I (and thousands of other investors) send direct mail to homeowners that have “high equity” in their property. My equity filter is 50%+. And that’s high! I know investors that are sending mail to people that just have 35% equity in their property.

?Is There a Right Way To “Buy In Cash?”

Needless to say, buying in cash is normal and plenty of people are doing it.

However, there are a few things you can do to avoid the mess I described above.

Does it take a little extra leg-work? Yes. But will it be worth it? Definitely.

Allow me to illustrate how to properly buy a property in cash by providing an example of an investor paying cash for a rental property held in an LLC.

✊?Putting This Strategy Into Action

I don’t have the money to be buying properties in cash, so I can’t speak to this with my own experience.

However, one of my friends recently bought a 3-family investment property with cash, so I’ll use his transaction to explain my method.

Let’s call my friend, Harry, and let’s call the LLC that owns his property 123 Main St LLC.

Harry bought the property for $470,000. He expects to invest another $15,000 on the rehab and he probably spends less than $15,000 on working capital. He’ll be all-in to this deal for right around $500,000.

Harry’s a straight baller, so he used cash from his checking account to fund the deal. When I heard about this, I called him up and walked him through everything you just read.

Here’s what I advised Harry to do next time:

- Open a business checking account for 123 Main St LLC.

- Transfer purchase money, rehab money, and working capital funds ($500,000) from Harry’s personal checking to 123 Main St LLC business checking.

- Write a Promissory Note from 123 Main St LLC to Harry the individual for the total expected investment: $500,000.

- Close on the property with funds from 123 Main St LLC business account.

- Ask the title company to record a mortgage for $500,000 from 123 Main St LLC to Harry the individual.

- Make your improvements to the property, get it appraised, and go for your refinance.

- If the appraisal comes back favorable and you can pull all your money out, go for a rate and term refinance.

- If the appraisal comes back less than favorable, pull out as much as you can and have the Harry the individual provide a payoff amount equal to the loan so it remains a rate and term refinance.

This sounds like overkill and a bit of a hassle, but it’s just good business. Ultimately, you’re protecting your equity and hedging against unnecessarily higher interest rates.

Harry and I are working together now to get a lien recorded against his property so when he does go for a refinance, he can get the best rate available.

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.